- Heart attack damage affects more than 55,000 Canadians every year, which can leave life-threatening impacts

- Heart attack is commonly covered under critical illness insurance policies

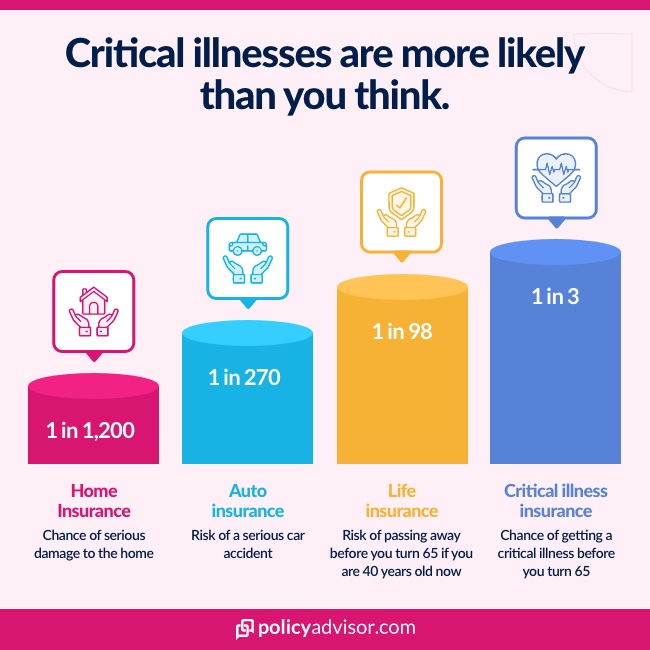

- Heart attacks are the second-most claimed health event under critical illness policies

- Critical illness insurance can help you cope with the financial and medical impact of a heart attack and other life-threatening conditions

Every year in Canada, roughly 63,200 people are diagnosed with a heart attack for the first time (source: Government of Canada). With the heart attack mortality rate of about 12% (source: Healthline), that means that every year over 55,000 people live with varying degrees of heart damage, which can impact lifestyle, mobility, and the ability to work.

Critical illness insurance can play a vital role in supporting people’s heart attack recovery by providing financial protection should they undergo this life-threatening health event. Critical illness insurance is a living benefit that can be used at the insured’s discretion, whether it’s to pay for care, treatment, income replacement, or anything else they may need. Keep reading to learn more about who is eligible for heart attack insurance and how it can protect your financial future.

Can I claim critical illness insurance for a heart attack?

Yes, you can typically claim critical illness insurance for a heart attack, but it depends on the policy terms. Most critical illness policies cover heart attacks, but they may specify severity levels or medical criteria that must be met, such as evidence of heart muscle damage or elevated cardiac enzymes.

Minor heart conditions might not qualify. It’s essential to review your policy’s definitions and exclusions to understand coverage details and ensure your claim aligns with the requirements.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is a heart attack?

A heart attack, also called myocardial infarction, is when the heart muscle suffers damage due to a lack of blood flow and, consequently, lack of oxygen. Just as a stroke is caused by loss of blood flow to the brain, a heart attack is caused by a lack of blood flow to the heart.

The severity of heart attacks varies depending on how long the blood supply is cut off from the vital organ. In worst-case scenarios, it can lead to cardiac arrest and death.

What are the probable causes of a heart attack?

There are several factors that can cause heart attacks. The most common cause is obstructed coronary arteries due to buildup of plaque, cholesterol plaque, or blood clots. Heart attacks can also be caused by a coronary artery spasm, which temporarily restricts the coronary artery, inhibiting blood flow.

While heart attacks are often unexpected, there are certain factors that influence your risk of heart disease—some of which can be mitigated. For instance, smoking, stress, recreational drug use, obesity, high blood pressure, and high cholesterol can all increase your risk of this medical condition. Other uncontrollable factors—such as age, family medical history, and certain autoimmune conditions—can contribute to your risk of a heart attack.

What is critical illness insurance?

Critical illness insurance is a type of coverage offered by life insurance companies (typically as an add-on to a life insurance policy, but can also be purchased as a stand-alone policy) that pays out a tax-free lump sum should the insured be diagnosed with a life-threatening illness or suffer a serious health event while the policy is active.

Unlike traditional life insurance, critical illness insurance issues a benefit while the insured is alive, providing them and their family with financial support as they manage the financial and health impact of a life-threatening illness. This money can be used to pay medical expenses, cover non-traditional treatment, travel expenses or any other expenses the family sees fit.

It should be noted that the critical illness insurance benefit is only paid if the insured is diagnosed with a covered illness, as specified in the policy. The proceeds of the insurance can be used fully at the discretion of the insured.

How does critical illness insurance work?

Critical illness insurance offers financial protection by paying out a tax-free lump sum if you are diagnosed with a covered condition. To activate the policy, you must:

- Be diagnosed with a specific illness listed in your plan (e.g., cancer, heart attack)

- Submit a claim with medical documentation

- Meet the waiting period requirements (if applicable)

The payout can be used for any purpose, including medical expenses, income replacement, or lifestyle adjustments during recovery.

Does critical illness insurance cover heart attack?

Yes, critical illness policies cover heart attacks. In fact, heart attacks are the second most claimed health event through critical illness coverage (representing 13%), following cancer (63%). If you’ve suffered from a heart attack, it is important to note what insurance companies consider when approving claims.

First, a heart attack requires a medical specialist diagnosis, and the insured must have undergone symptoms as well as electrocardiogram (ECG) changes that are consistent with a heart attack.

How much does critical illness insurance cost?

Critical illness insurance can cost between $22 and $921 per month depending on factors like age, health, coverage amount, and policy term. For example, A 25-year-old male non-smoker could pay $22.49 per month for $100,000 coverage over 10 years and $56.70 per month for $250,000 coverage over 20 years.

Critical illness insurance premiums across different categories

| Category/Coverage Period and Amount | 10 Years ($100,000) | 20 Years ($100,000) | 10 Years ($250,000) | 20 Years ($250,000) | 10 Years ($500,000) | 20 Years ($500,000) |

| Male Non-Smoker (Age 25) | $22.49 | $26.82 | $48.09 | $56.70 | $90.21 | $108.00 |

| Male Non-Smoker (Age 35) | $30.87 | $42.50 | $68.40 | $96.75 | $130.81 | $187.25 |

| Male Non-Smoker (Age 45) | $63.18 | $89.78 | $136.35 | $214.82 | $267.30 | $423.66 |

| Male Non-Smoker (Age 55) | $153.81 | $234.09 | $321.75 | $470.02 | $638.10 | $921.15 |

| Female Non-Smoker (Age 25) | $24.20 | $27.09 | $47.88 | $57.83 | $91.49 | $110.25 |

| Female Non-Smoker (Age 35) | $32.07 | $44.04 | $69.47 | $100.04 | $132.95 | $195.37 |

| Female Non-Smoker (Age 45) | $62.01 | $81.74 | $135.45 | $194.73 | $266.40 | $383.47 |

| Female Non-Smoker (Age 55) | $127.06 | $173.70 | $285.98 | $408.60 | $567.45 | $801.00 |

Is critical illness insurance tax deductible?

The payout from a critical illness policy is tax-free. However, the premiums paid by individual policyholders, are considered a personal expense and are not tax deductible. For businesses providing critical illness coverage to employees, the premiums may be deductible as a business expense.

How to claim critical illness insurance?

To claim your critical illness insurance, you need to submit a claim form to your provider within their specified timeframe. For instance, companies like Canada Life and RBC require you to submit your claim form along with satisfactory proof of diagnosis within 30 to 90 days of the diagnosis date or surgery.

Can I be denied critical illness claim for a heart attack?

There can be certain scenarios in which your critical illness claim may be denied. For instance, a claim may be denied if a policyholder has ECG changes that point to a pre-existing heart attack, displays other acute coronary syndromes, or has undergone a medical procedure or received another diagnosis that has caused elevated cardiac biomarkers.

How long do I have to wait to file a claim after having a heart attack?

In order to make a claim for heart attack insurance, policyholders must be diagnosed with a heart attack by a physician and wait 30 days after the diagnosis. This waiting period is called a survival period. Some insurance providers do offer shorter survival periods. Typically, the critical illness benefit will be paid within a month of the claim being submitted.

Can I start a critical illness insurance policy after I’ve had a heart attack?

While it is much easier to start a critical illness insurance policy before suffering any major health events, it is still possible to find coverage after a heart attack recovery. In other words, you have options, though you may not qualify for the most competitive rates or highest benefits.

The most common route for those who have recovered from a heart attack is guaranteed critical illness insurance. This type of policy, though inclusive, has some limitations. For example, guaranteed critical illness insurance typically includes a two-year pre-existing condition exclusion.

This means that if you’ve suffered from a heart attack in the two-year period before the start of the policy, any heart attack or related health event in the next two years will not be covered.

Can I get critical illness insurance if my family has cardiovascular health concerns?

If your family has a history or signs of heart disease, it is prudent to think about investing in critical illness insurance. Though most life insurance companies take family medical histories into account when evaluating a critical illness insurance application, having an increased risk of heart disease will not necessarily exclude you from coverage. Your coverage limit and premium rates, however, may be impacted.

In cases where family history is a consideration, it is advisable to purchase critical illness insurance sooner rather than later. This will increase your chances of being able to place coverage and improve the premium rates you are offered.

To find out more about insurance for heart attacks and other critical health conditions, head to our critical illness insurance learning centre. To better understand how much critical illness insurance coverage you might need, consult our critical illness insurance calculator.

How to get the best critical illness quotes in Canada?

Finding the best critical illness insurance quotes in Canada can be a hassle, but PolicyAdvisor makes it simple and stress-free. With the help of our experienced advisors, you can compare rates from Canada’s top insurance providers, offering side-by-side comparisons of critical illness plans tailored to your needs.

Whether you’re looking for broad coverage, competitive premiums, or specific illness inclusions, PolicyAdvisor can help you curate options based on your unique requirements.

Frequently asked questions

How does critical illness insurance differ from disability insurance when covering heart attacks?

Critical illness insurance provides a one-time lump sum payment upon diagnosis of a covered condition, like a heart attack, while disability insurance replaces a portion of your income if you’re unable to work due to any medical condition. If your heart attack meets the criteria outlined in your critical illness policy, you’ll receive the payout regardless of your ability to continue working.

Does critical illness insurance cover rehabilitation costs after a heart attack?

The lump sum payout from critical illness insurance can be used for any purpose, including rehabilitation, medical expenses, lifestyle adjustments, or even paying off debt. Unlike health insurance, it doesn’t reimburse specific medical costs—it gives you the flexibility to allocate the funds where you need them most.

What happens if I have multiple heart attacks?

Most critical illness policies provide a one-time lump sum payout per insured condition. If you suffer multiple heart attacks, only the first eligible claim will be covered. However, some policies offer multi-condition coverage or allow for separate claims if different critical illnesses occur.

Can I purchase critical illness insurance if I already have a heart condition?

If you have a pre-existing heart condition, insurers might exclude heart attacks from your coverage or charge significantly higher premiums. Some specialized policies cater to individuals with pre-existing conditions, though the terms might be more restrictive. Check out your policy documents to find out whether your insurance policy covers heart attack as a pre-existing condition.

Critical illness insurance policies may cover up to 26 diseases or illnesses. This insurance provides a lump-sum payment if you should be diagnosed with one of these illnesses. Heart attack is commonly covered under most critical illness insurance plans.