- Employee benefits for small businesses in Canada typically range from $150 to $275 per employee per month, depending on the type of coverage offered

- Offering health benefits can lead to improved employee satisfaction, with 79% of employees prioritizing health insurance over other compensation

- Small businesses can manage employee benefits costs effectively through strategies like leveraging virtual health care and optimizing benefit structures based on employee needs

Offering employee benefits is one of the most effective ways for small businesses in Canada to attract and retain top talent. According to the Canadian Life and Health Insurance Association (CLHIA), 68% of all health insurance coverage in Canada is provided through group insurance plans, underscoring the importance of group benefits.

Several factors may influence the cost of employee benefits in Canada, including company size, employee age, industry type, and claims history. On average, small business employee benefits cost $150 per employee/month for basic coverage, $205 for standard plans, and up to $275 for enhanced options.

In this guide, we explain how small businesses can find cost-effective group benefits plans tailored to their budget and employee needs. Read on to learn about small business employee benefits costs in Canada.

How much does Group Insurance cost?

Get instant quotes from Canada's top group insurance providers and find the perfect coverage for your business.

Powered by

![]()

What are small business group benefits?

Employee benefits are non-wage benefits or compensation given to employees in addition to their regular salaries. For small businesses in Canada, these benefits typically include health insurance, dental care, life insurance, disability coverage, and other perks like mental health support and retirement plans.

Offering employee benefits can significantly improve employee satisfaction and retention. In a competitive job market, employees often prioritize employers who provide comprehensive health and wellness benefits over those who do not.

Here are some common small business employee benefits packages in Canada:

- Group health insurance: Provides coverage for medical expenses, including hospital visits, surgeries, and prescription medications

- Dental and vision coverage: Covers cleanings, fillings, eye exams, and prescription eyewear

- Mental health coverage: Offers access to mental health services, including counselling and therapy, promoting overall emotional well-being

- Life and disability insurance: Offers financial protection in case of death, critical illness, or long-term disability

- Employee Assistance Programs (EAPs): Provide access to counselling, addiction support, and stress management resources

- Retirement savings plans: Include group registered retirement savings plans (RRSPs), deferred profit sharing plans (DPSPs), or pension plans with optional employer contributions

- Wellness perks: Can feature gym memberships, mental wellness apps, paid mental health days, or remote work options

- Health spending accounts: Health spending accounts (HSAs) allow employers to reimburse employees tax-free for eligible medical, dental, or wellness expenses not covered by public plans

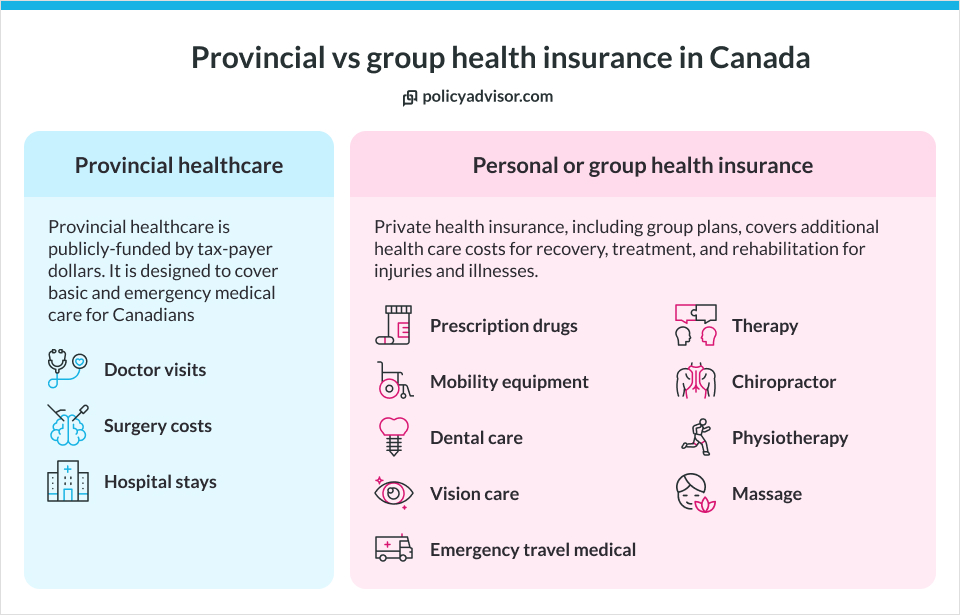

What does a group insurance plan for a small business look like?

A group plan provides affordable coverage to the employees and their dependants. Group benefits plans are typically available in Basic, Standard, and Enhanced options.

When it comes to providing employee benefits for small businesses, offering benefits such as health insurance, which provides extended coverage for medical expenses, and dental care, can positively impact your workforce’s health. Additionally, options like vision care, travel insurance, and disability insurance are also crucial for financial security.

Below is a breakdown of what coverage is typically offered in group insurance for your employees:

| Coverage | Basic | Standard | Enhanced |

| Drug maximum | $5,000/person | $10,000/person | Unlimited/person |

| Paramedical services | $300/practitioner | $500/practitioner | $1,000/practitioner |

| Vision care | N/A | $150/person for

24 months |

$300/person for

24 months |

| Dental (Basic & Major) | $700 combined | $1000 combined | $1500 combined |

| Dental coinsurance | 50% | 50% | 80% |

| Recall exam | 1 every 9 months | 1 every 6 months | 1 every 6 months |

| Pooled benefits

(Life Insurance) |

$25,000 | $50,000 | $75,000 |

| Health Spending Account

(HSA) |

As requested | As requested | As requested |

| Travel insurance | Yes | Yes | Yes |

How much does a small business’s benefits package cost per employee in Canada?

The table below illustrates the typical group benefits cost per employee for basic, standard, and enhanced plans:

| Benefits | Basic plan | Standard plan | Enhanced plan |

| Health coverage | |||

| Employees – Single | $50/month | $70/month | $92/month |

| Employees – Couple | $98/month | $130/month | $180/month |

| Employees – Family | $110/month | $170/month | $195/month |

| Dental coverage | |||

| Employees – Single | $30/month | $60/month | $81/month |

| Employees – Couple | $100/month | $128/month | $140/month |

| Employees – Family | $170/month | $200/month | $250/month |

| Pooled benefits | |||

| Life insurance & AD&D | $12/month ($25,000) | $18/month ($50,000) | $26/month ($75,000) |

| Critical illness | Not selected | Not selected | Not selected |

| Long-term disability | Not selected | Not selected | Not selected |

| Total monthly premium | $3,000/month | $4,100/month | $5,500/month |

| Cost of benefits per employee | $150/month | $205/month | $275/month |

*This table provides an indicative cost for a small business that has 20 employees.

What is the cost of group benefits for employers as a percentage of payroll?

The average annual premium for small business group benefits typically varies based on the size of the business. For smaller businesses, the cost usually ranges from 10-20% of payroll, reflecting their more limited risk pools and potentially higher per-employee costs.

In contrast, larger companies may see higher total premiums due to their larger risk pools and more extensive benefit offerings. However, there are cost-effective options available for small businesses, where group insurance plans can be customized to fit tighter budgets, costing as little as 5% to 10% of payroll. This flexibility allows small employers to provide valuable benefits without overwhelming their financial resources.

What factors affect employee benefit costs for small businesses?

Factors such as employee demographics, type of coverage, claims history, business location, employee–employer cost share, and industry affect small business health insurance costs.

- Business size and workforce demographics: The number of employees and their ages, health conditions, and family size influence benefit costs, as larger or older workforces typically result in higher premiums

- Type and extent of coverage: Offering more comprehensive benefits, such as dental, vision, disability, or prescription drug coverage, increases costs compared to basic health plans

- Location and industry: Regional health care costs and the industry in which the business operates can impact benefit expenses. Some regions or industries may face higher premiums due to risk factors or local health care costs

- Claims history: A company’s history of claims affects its premiums, as frequent or high-value claims may lead to increased costs in subsequent years

- Plan design and contributions: The way a plan is structured, including deductible amounts, copayments, and employer-employee contribution splits, plays a key role in determining the overall cost of benefits

Are employee benefits worth the cost for small businesses?

According to a survey by Benefits Canada, 79% of employees would prefer employee benefits over an appraisal, and the most preferred benefit is health insurance. Many small businesses in Canada thus view it as a valuable investment rather than just a cost. It offers the following benefits:

- Improves employee satisfaction: Offering employee benefits can significantly improve employee satisfaction and retention. In a competitive job market, employees often prioritize employers who provide comprehensive health and wellness benefits over those who do not

- Promotes a more productive workforce: Access to health care services, mental health support, and preventive care through group benefits can help employees address health concerns early. This not only supports employee well-being but can also minimize disruptions to business operations and improve overall productivity

- Offers tax benefits: Employee benefits also offer tax benefits to both employers and employees. Premiums paid by employers for health and dental benefits are generally tax-deductible expenses, and many health benefits are received tax-free by employees

How can small businesses lower the costs of employee health benefits?

Managing employee health benefits can be challenging for small businesses in Canada; however, by reducing prescription drug costs and incorporating government programs, small businesses can offer competitive benefits while keeping expenses under control.

Here are a few things small businesses can do to manage the costs of employee benefits:

- Cap prescription drug costs: Implementing caps on drug coverage or exploring hybrid spending accounts to manage rising prescription drug costs

- Incorporate virtual healthcare: Virtual health care services allow employees to consult with health care professionals online, reducing the need for in-person visits. Many insurers now include virtual care as part of group plans, improving access to health care

- Invest in preventive care: Wellness programs reduce long-term health care costs by promoting healthier lifestyles and preventing chronic diseases

- Join pooled benefits: Small businesses can join pooled benefit plans or industry association plans, which combine multiple businesses into a larger risk pool. This allows insurers to spread risk across more employees, often resulting in more stable premiums and better coverage options

Do employee benefits costs increase each year?

Employee benefits premiums are typically reviewed once a year at renewal, and it is common for costs to fluctuate during that time. Some of the factors affecting the change in premium include:

- Claims utilization: If a group consistently submits higher claims for services such as prescription drugs, dental care, or paramedical treatments, insurers may increase premiums to reflect the higher level of usage. This is experience-based pricing, where renewal rates are influenced by the group’s past claims activity

- Rising health care costs: Increases in prescription drug prices and health care services can raise the overall cost of providing benefits, hence affecting the premiums

- Employee demographics: As the average age of employees increases, the likelihood of medical claims may rise, which may result in increased premiums

Which are the cheapest group benefits plans available for small businesses?

Group health benefits plans for small businesses in Canada can start as low as $70–$90 per employee per month, depending on factors such as team size, employee demographics, and plan design. These entry-level plans typically include basic health and dental coverage, with options to scale benefits as the business grows.

Costs are kept low through plan design choices such as:

- Lower annual maximums for health and dental services

- Basic drug coverage, often with caps

- Use of flexible options like Health Spending Accounts (HSAs) to control employer costs

Some of the top insurance companies in Canada offering affordable group benefits plans include GreenShield, Empire Life, Manulife, and a few others. Small businesses can explore these insurers, along with various other options available, to find a plan that meets their budget while still providing valuable protection for their employees

How to get the cheapest group benefits insurance quotes in Canada?

Finding affordable group benefits insurance for your small business doesn’t have to be complicated. With PolicyAdvisor, you can secure comprehensive employee coverage at competitive rates.

At PolicyAdvisor, we make the process quick and hassle-free. You can rely on us to:

- Compare quotes from 30+ leading Canadian insurers in one place

- Get personalized group benefits quotes in under 60 seconds

- Tailor your plan to meet the specific needs of your employees and budget

- Speak with licensed advisors for expert guidance on the best coverage

- Rely on after-sales support, including claims assistance and plan updates

Whether you are a startup or an established small business, PolicyAdvisor helps you find the best group insurance plan at the lowest possible rate. Schedule a call with us today to get the best employee insurance quotes.

Frequently Asked Questions

Which employee benefit do employees value the most?

Health and dental insurance are often considered the most valued benefits among employees. Group health insurance provides more extensive coverage than provincial health plans.

What are the best small business employee benefits insurance companies?

Top providers include Manulife, Sun Life Financial, and Canada Life, recognized for their comprehensive offerings and competitive pricing.

How do employee demographics impact the cost of group benefits?

Employee demographics significantly affect group benefit costs; younger employees generally incur lower health care costs compared to older employees, which influences premiums.

What is the average cost per employee as a percentage of payroll for employee benefits in Canada?

On average, the small business health insurance costs per employee are around 10%-20% of payroll, including both mandatory and supplementary benefits.

How can small businesses balance benefit costs with employee satisfaction?

Small businesses can balance benefit costs with employee satisfaction by offering flexible options that allow employees to choose benefits that suit their needs, promoting wellness programs to reduce long-term health care costs, and encouraging cost-sharing through copayments or deductibles. Focusing on key benefits like health and dental, and regularly communicating the value of the benefits package, can enhance employee appreciation and satisfaction.

Are employee benefits tax-deductible in Canada?

Yes, group benefits provided by an employer are generally tax-deductible in Canada. Employers can deduct the cost of providing group benefits, such as health and dental insurance, from their business income when calculating their taxable income.

However, tax treatment can vary depending on the type of benefit and the province, so employers should confirm details with a tax professional to ensure they are complying with the specific rules and requirements for deducting group benefits.

The cost of small business employee benefits in Canada typically ranges from $150 to $275 per employee per month, depending on the plan design. Factors influencing these costs include the number of employees, their demographics, industry type, and claims history. The most common benefits included in these packages are health insurance, dental care, vision care, life insurance, and disability coverage.

Canadian Life and Health Insurance Association. Fact Book 2023. Toronto: CLHIA, 2023