- Small businesses in Canada can choose between basic, standard, and enhanced group benefits plans, each offering different levels of coverage

- Group insurance includes coverage for health, dental, life, and disability insurance, along with employee assistance programs (EAPs) and wellness programs

- Providing employee benefits helps small businesses improve employee satisfaction, retention, and productivity

- The cost of group benefits is affected by factors such as coverage levels, employee demographics, type of group benefits, and more

In an increasingly competitive job market, offering group benefits in Canada has become a strategic tool for attracting, retaining, and supporting employees. According to Employee Benefits Statistics Canada, 89% of Canadians prefer employee benefits for their financial security.

From health and dental coverage to additional options like health care spending accounts (HSAs) and wellness-focused programs, small business owners now have a wide range of options to choose from in their small business group benefits package.

In this guide, we will break down the different types of small business group benefits packages available in Canada.

How much does Group Insurance cost?

Get instant quotes from Canada's top group insurance providers and find the perfect coverage for your business.

Powered by

![]()

What are the different types of group benefits plans that small businesses can choose from?

Small businesses can choose from different tiers of group benefits that most Canadian insurers offer. Typically known as basic, standard, and enhanced plans, these packages include health, dental, and vision care, along with optional life insurance, accidental death and dismemberment (AD&D) coverage, and health spending accounts (HSAs). These plans differ based on coverage limits, reimbursement levels, and included benefits.

Basic plan

Basic plans are designed to provide essential coverage at the lowest possible cost. They typically include limited health and dental benefits and may include additional benefits such as disability and critical illness insurance. Basic plans are mostly chosen by:

- Startups or very small teams

- Businesses offering benefits for the first time

- Employers prioritizing affordability over comprehensiveness

Standard plan

Standard plans offer a balance of coverage and premium affordability. They expand on basic plans by increasing coverage limits, improving reimbursement levels, and adding more comprehensive benefits. They are ideal for:

- Growing businesses

- Employers who want to offer comprehensive coverage

Enhanced plan

Enhanced plans provide comprehensive, high-limit coverage for benefits such as health and dental insurance, life insurance, critical illness insurance, and travel insurance. Depending on the insurer, some of these coverages can be optional. This plan is best suited for:

- Established small businesses

- Employers focused on retention and employee experience

The following table outlines different types of employee benefits packages and their benefits, with indicative coverage based on typical coverage options.

Different types of small business employee benefits plans

| Feature | Basic plan | Standard plan | Enhanced plan |

| Prescription drugs | $2,500 – $5,000/year | $10,000 – $25,000/year | $100,000/year – Unlimited |

| Co-insurance (Drugs) | 70% | 80% | 90% – 100% |

| Paramedical practitioners | $200 – $350/practitioner | $500 – $750/practitioner | $1,000 – $1,500/practitioner |

| Co-insurance (Practitioners) | 50%-70% | 70%-80% | 80%-100% |

| Vision coverage | Nil – $150/2 years | $150 – $200/2 years | $250 – $300/2 years |

| Dental (Basic) | $750 – $1,000 | $1,250 – $1,500 (combined) | $2,500 (combined) |

| Dental (Major) | Nil | Nil – $1,000 (combined) | $1,500 – $2,500 (combined) |

| Co-insurance (Dental) | 50% – 70% | 80% (for basic)

50% (for major) |

80% (for basic)

50% (for major) |

| Life insurance | Nil | $10,000 – $25,000 | $50,000 – $75,000 |

| Accidental death & dismemberment (AD&D) | Nil | $10,000 – $25,000 | $50,000 – $75,000 |

| Travel insurance | 60-day trips | 60-day trips | 90 to 180-day trips |

| Health Spending Account (HCSA) | $500 | $1,000 – $2,000 | $3,000 – $5,000 |

| Rate guarantee (optional) | 16 – 28 months | 16 – 28 months | 28 months |

*Illustrative coverage amounts for 8 employees, and actual numbers can vary depending on the provider, the number of employees, and the specific coverage selected.

What are the most common group benefits offered to small business employees?

Most employers commonly offer health, dental, life, and disability insurance under their group benefits for a small business package. Some employers may also offer Employee Assistance Programs (EAPs), Health Spending Accounts (HSAs), and other wellness benefits.

These benefits are designed to support both the physical and financial well-being of employees, fostering a healthier and more motivated workforce. The most common group benefits include:

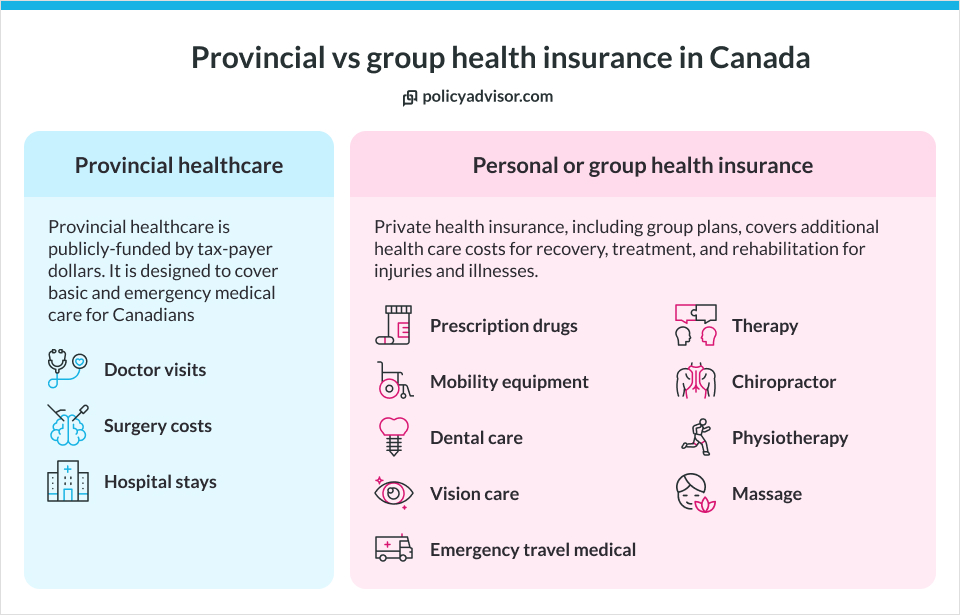

- Health insurance: This extends coverage beyond the provincial healthcare system and typically includes expenses for prescription drugs, vision care, paramedical services like physiotherapy, chiropractic care, and mental health services

- Dental insurance: Dental plans usually cover routine dental services such as cleanings, fillings, and preventive care. More comprehensive plans may also include coverage for orthodontics, major dental work, and surgeries

- Life insurance: In the event of an employee’s death, life insurance provides a financial safety net for their beneficiaries. This payout helps cover funeral costs, and outstanding debts and provides income replacement for the family

- Disability insurance: Disability coverage ensures that employees who are unable to work due to illness or injury receive a portion of their income during recovery

- Employee Assistance Programs (EAPs): EAPs offer confidential counselling and support services for personal, financial, or work-related challenges

- Health Spending Accounts (HSAs): If a business’s budget allows, offering a Health Spending Account can be a flexible way to provide additional healthcare benefits. HSAs give employees a set amount of funds to use for eligible health-related expenses not covered by traditional insurance, such as extended paramedical services or wellness programs

- Critical illness insurance: This provides employees with a tax-free lump-sum payment if they are diagnosed with a covered serious condition

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What do small business employee benefits packages look like?

A small business’s employee benefits plan typically includes health, life, dental, AD&D, and travel insurance, along with HSAs, wellness benefits, and other extended health care coverage.

Here’s a sample employee benefits plan for a small business with 10 employees:

| Benefit | Details |

| Health insurance | |

| Prescription drugs | Up to $10,000/year with 80% co-insurance |

| Paramedical practitioners | $500 per practitioner/year with 80% co-insurance |

| Vision coverage | Up to $200 every 2 years |

| Dental coverage | |

| Basic dental | $1,250 per employee (combined) with 80% co-insurance |

| Major dental | Up to $1,500 per employee (combined) with 50% co-insurance |

| Life insurance | $25,000 per employee |

| Accidental Death & Dismemberment (AD&D) | $25,000 per employee |

| Health Spending Account (HCSA) | $1,000 per employee/year |

| Travel insurance | Coverage for up to 60-day trips for business-related travel |

| Employee Assistance Programs (EAPs) | Confidential counselling services |

| Wellness programs | Annual reimbursement of up to $300 per employee for fitness-related expenses |

| Monthly premiums | |

| – Health Insurance | Approximately $500 per employee (total: $5,000/month) |

| – Life Insurance | Approximately $25/month per employee (total: $250/month) |

| – AD&D Insurance | Approximately $10/month per employee (total: $100/month) |

| Total estimated monthly cost | $5,350 |

| Total annual cost | $64,200 |

*Note that these are illustrative costs for 10 employees, and actual numbers can vary depending on the provider, the number of employees, and the specific coverage selected.

What is the cost of a small business employee benefits package?

The cost of small business employee benefits package depends on factors like the number of employees, the type of coverage offered, employee demographics, and more. Most group plans are customizable, and the cost varies accordingly.

Here is a table depicting the small business health insurance costs on the basis of the number of employees and plan type.

Total monthly cost of group insurance for small businesses

| Employee count | Basic plan | Standard plan | Enhanced plan |

| 15 employees | $1,185/mo | $1,380/mo | $2,025/mo |

| 30 employees | $2,370/mo | $2,760/mo | $4,050/mo |

| 45-50 employees | $3,752.5/mo | $4,370/mo | $6,412.5/mo |

*Illustrative costs for different plan tiers. Actual cost will vary based on plan design, company details, and employee demographics.

How does the choice of benefits affect the cost of group benefits for small businesses?

The type of benefits package you choose, whether basic, standard, or enhanced, has a direct impact on your group insurance premiums. Basic plans cost less because they offer limited coverage, while enhanced plans cost more because they provide wider benefits.

Factors like employee demographics, type of coverage, claims history, location of business, and industry affect the cost of employee benefits for small businesses. Additionally, the benefits an employer chooses also impact the premiums. Let us see how:

- Addition of disability coverage: Disability insurance is one factor that can significantly affect your premiums. Adding short- or long-term disability coverage can increase the overall cost of your benefits package since it ensures employees are covered for lost wages due to injury or illness

- Prescription drug coverage: Higher prescription drug limits and co-insurance percentages will drive up premiums. For example, a plan offering unlimited prescription drug coverage and 100% co-insurance will be considerably more expensive than one with a lower drug limit and a 70-80% co-insurance rate

- Dental and vision care: Plans offering major dental and high-coverage vision care (such as exams and glasses) typically come with higher costs. If your workforce places a high value on comprehensive dental and vision coverage, investing in an enhanced package may lead to better retention but at a premium

- Healthcare spending accounts (HSAs): Offering a healthcare spending account gives employees flexibility to cover additional healthcare costs, but larger HSAs increase the total package cost. Small businesses often opt for a moderate HSA allocation to balance the cost with employee satisfaction

- Paramedical coverage: Offering a higher level of paramedical coverage for physiotherapists and chiropractors, massage therapists, naturopaths and psychologists increases the group benefit package cost

- Life insurance: Many insurance companies offer life insurance as an additional benefit in their employee benefits package. Insurers that include life insurance as a core benefit will cost more than those offering it as an optional benefit

How do small business employee benefits packages compare to those of larger companies?

Health benefit plans for small businesses often exhibit distinct differences compared to those provided by larger companies. Small businesses typically offer more standardized plans with limited negotiating power, resulting in higher premiums per capita and a focus on basic coverage options.

In contrast, larger companies benefit from greater customization, enhanced negotiating power, lower premiums through economies of scale, and the ability to provide comprehensive packages that may include wellness programs.

Differences between group plans for small businesses and large corporations

| Feature | Small businesses | Larger companies |

| Plan customization | Typically more standardized due to a smaller employee base | Highly customizable to meet diverse employee needs |

| Negotiating power | Limited negotiating power with insurers | Greater leverage due to larger employee pools |

| Cost structure | Higher premiums per capita due to smaller risk pools | Lower premiums achieved through economies of scale |

| Types of benefits offered | Basic coverage options | Comprehensive packages that often include wellness programs |

How to choose the best group benefits plan for a small business?

Choosing the best health insurance for a small business depends on aligning your coverage with your employees’ needs, your budget, and your long-term business goals. The following factors can help you choose the best group benefits plan:

- Employee demographics: The age, family status, and healthcare preferences of your employees influence which benefits will be most valuable, as younger teams may prioritize services like mental health support, while an older workforce may place greater emphasis on comprehensive health and critical illness coverage

- Budget: Your available budget plays a crucial role in determining the type of plan you can offer, as enhanced plans typically come with higher premiums compared to basic plans, making it important to balance coverage with your budget

- Coverage: Choose the coverage that your employees value most. As per a survey, the most preferred coverage is health and dental. You can also enhance the coverage with additional benefits like life insurance, critical illness insurance, disability insurance, and a few others

- Flexibility: The ability to customize and adapt the plan over time is essential, as a flexible benefits package allows you to adjust coverage based on changing employee needs and the growth of your business

How can small businesses get affordable employee benefits packages?

Small businesses seeking affordable employee benefits packages can consider pooled benefits, tiered plans, and HSAs to ensure they provide valuable coverage without straining their budgets. Pooled benefits are effective and allow multiple small businesses to come together to share the costs and risks associated with insurance.

Pooled benefits result in more predictable and often lower premium costs for each business involved in the pool. By sharing the burden of claims, small businesses can enjoy comprehensive coverage at a fraction of the cost they would face individually.

In addition to pooled benefits, small businesses should also:

- Consider Health Spending Accounts (HSAs): These accounts allow employees to manage their health expenses tax-efficiently and can be a cost-effective addition to traditional benefits

- Implement wellness programs: Promoting wellness initiatives can reduce overall healthcare costs by encouraging healthier lifestyles among employees, which may lead to fewer claims

- Offer tiered plans: Providing different levels of benefits allows employees to choose what suits them best, which can help manage costs while still offering valuable options

- Speak to PolicyAdvisor’s licensed advisors: Our experienced advisors help you compare quotes from across 30+ Canadian insurers to find the best small business employee benefits rates for your company

Frequently Asked Questions

Does your small business need to offer employee benefits?

Yes, small businesses in Canada must consider providing employee benefits, especially in today’s competitive job market. As per a Pacific Blue Cross report, around 72% of Canadian small businesses offer benefits, acknowledging the valuable returns these plans offer through increased employee satisfaction, retention, and productivity.

How much do group health benefits cost per employee in Canada?

On average, the cost of employee benefits in Canada can range between $80-$200 per month per employee for a very basic plan, $100-$250 per employee for a standard plan, and $150-$350 for an enhanced plan. This includes benefits like health insurance, dental care, and life insurance. The actual cost will depend on various factors, including the size of the workforce, the specific benefits offered, and the overall compensation strategy of the business.

What is the minimum number of employees required to qualify for group benefits?

You need at least two employees to qualify for group health benefits. Some group plans allow flexibility for small businesses to start with a minimal number of employees and gradually expand coverage as the company grows.

Can part-time or contract workers be included in group plans?

Yes, part-time or contract workers can be included in group benefit plans, but it depends on the specific policy and plan design. Employers may choose to extend coverage to these workers, especially if they want to offer competitive benefits to attract and retain diverse talent. However, eligibility requirements, such as minimum working hours, may apply.

What are the tax implications of providing group benefits?

The employer’s share of premiums for health, dental, and vision insurance is generally not considered a taxable benefit for employees. However, life insurance and certain other benefits may be treated as taxable income. Tax treatment can vary by province, so it’s essential to consult with a tax expert to ensure compliance and optimize your tax benefits.

How often can I change or update the benefit plans?

Group benefit plans can be reviewed and updated annually, usually during the renewal period. Changes can include adjusting coverage options, adding new benefits, or modifying employee cost-sharing arrangements. Employers should work closely with their benefits provider to determine the best time for any updates based on business needs and budget.

Approximately 72% of Canadian small businesses recognize the importance of providing group benefits, which can lead to increased employee satisfaction, loyalty, and productivity. This blog outlines the most common types of employee benefits, including health, dental, life, and disability insurance, and explores various group benefits plans available for small businesses. It also highlights ways in which small business owners can make group health insurance more affordable.