1-888-601-9980

1-888-601-9980

- Business owners can use whole life insurance as a source of liquidity to achieve diverse estate planning goals

- A business owner may purchase life insurance personally or through his corporation

- A corporation may purchase life insurance policies to facilitate key man insurance, buy-sell agreements, or estate equalization

- While there are several benefits and flexible planning opportunities, there are also a number of additional complexities to consider for corporate-owned life insurance

Life insurance can offer unique benefits to business owners and high-net-worth individuals. Alongside the traditional death benefit provided through a life insurance policy, permanent life insurance policies can be used to cover high tax bills, to secure a business loan, to help effectively plan an estate, and more.

In this article, we discuss what corporate-owned life insurance is and the many different ways it can benefit business owners and high-net-worth individuals in Canada.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is corporate-owned life insurance?

Corporate-owned life insurance (COLI) is a life insurance policy that is owned by a business or corporation rather than an individual. In this setup:

- The business owns the life insurance policy

- The covered person is a key person, such as an owner, shareholder, or vital employee

- Insurance premiums are paid with the company’s after-tax dollars, helping to maximize tax efficiency

- The business is the beneficiary, so the death benefit payout is made to the company — not the covered person

- In Canada, most COLI policies are permanent life insurance, a type of coverage that lasts permanently, builds cash value over time, and can pay out dividends

Corporate-owned life insurance is also called business life insurance or business-owned life insurance. Companies are allowed to own an insurance policy on an employee or key person once they have insurable interest.

What are the advantages of corporate ownership of a life insurance policy?

A corporate-owned life insurance policy has several advantages:

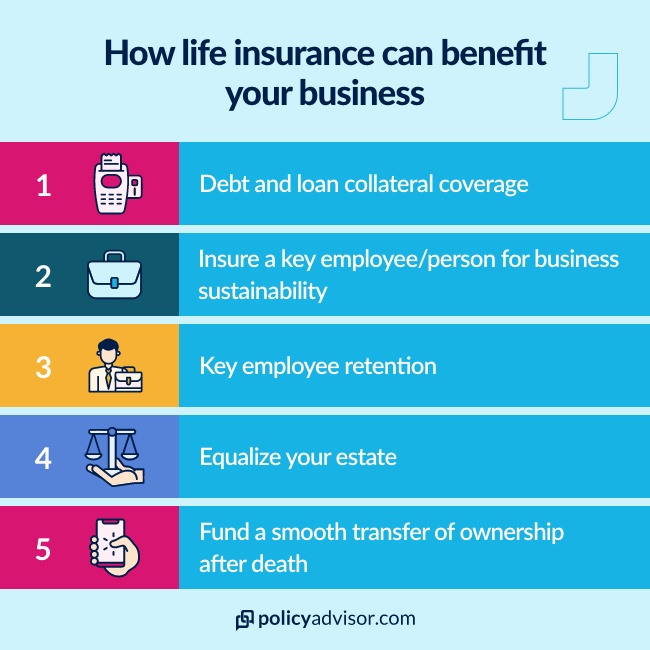

How can life insurance policy be used for your business?

There are multiple ways a business owner can leverage life insurance in Canada to ensure their business will continue after you pass away:

- Key person insurance

- Buy-sell agreements

- Estate equalization

- Life insurance collateral assignment

What’s the biggest risk of business-owned life insurance?

The biggest risk of business-owned life insurance occurs when a business ends up with a significant tax liability. This can happen if a shareholder passes away without a spouse to rollover their shares.

- When this happens, the deceased shareholder is deemed to have disposed of their shares at something called Fair Market Value (FMV)

- The cash surrender value (CSV) on the shareholder’s policy is included when computing the FMV of the shares

- When a business owns an insurance policy with a high CSV, the FMV of the shares of the deceased shareholder is also high

- As a result, the deceased shareholder will be subject to a large capital gain on death, and also a major tax liability

However, this tax liability can be avoided with something called insurance tracking shares.

What are insurance tracking shares?

Insurance tracking shares are a special kind of share issued to the heirs of an estate — this is usually the business owner’s child. It tracks the cash value of a COLI policy, but does NOT grant the shareholder (i.e. the deceased owner’s child) entitlement to dividends, proceeds on the sale of the business, or voting rights.

Learn more about corporate-owned life insurance in Canada

PolicyAdvisor’s licensed insurance experts can help you better understand what insurance products may be best for your situation and business. Book some time with us and see how you can use insurance to best plan for the future of your business, your estate, and your family’s future.

A business can own a life insurance policy as a way to ensure the continued viability and profitability of their business, while benefiting from the policy’s unique tax treatment. Life insurance is an effective tax and estate planning tool, especially for business owners. They can use it to protect their families, safeguard their personal and business assets, and support business continuity.