- The Canadian government had proposed to increase the capital gains inclusion rate from 50 percent to 66.7 percent for any profits above $250,000. The increased inclusion rate was to come into effect from June 25, 2024, but it has been deferred indefinitely.

- Currently, when you make a profit on the sale of an asset, half of that is counted as taxable income. Simply put, you pay taxes on 50 percent of your capital gain

- The proposed change is expected to impact both individuals and corporations and individual taxpayers would continue to pay tax on 50 percent of their capital gains up to $250,000 after the change comes into effect

The federal government’s proposed changes to capital gains taxes have received mixed reactions from the Canadian public and finance experts alike. While the conversations about the government’s proposal will continue to flash on our news screens, we’ve taken this opportunity to decode what the changes are and how they can impact corporations and individuals.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What are capital gains?

Capital gains are the profit you make when selling a valuable asset. When you sell something of value—real estate, stocks, bonds, ETFs, bonds, cryptocurrencies, or other investments—for an amount that is higher than the price you originally paid for it, the profit you receive is a capital gain.

Currently in Canada, when you make a profit on the sale of an asset (other than your principal residence), half of that is counted as taxable income. Simply put, you pay taxes on 50 percent of your capital gain.

The newly proposed changes to capital gains taxation are about to alter this.

What is the inclusion rate for capital gains in Canada?

In Canada, the inclusion rate refers to the percentage of capital gains that are included in an individual’s taxable income for the year. Prior to the recent announcement, the inclusion rate for capital gains in Canada was 50 percent. This meant that only half of the capital gains are subject to taxation.

For example, if you have a capital gain of $500,000, only $250,000 of that gain would be included in your taxable income. The proposed alterations to capital gains taxes are about to change this.

What are the proposed capital gains tax changes?

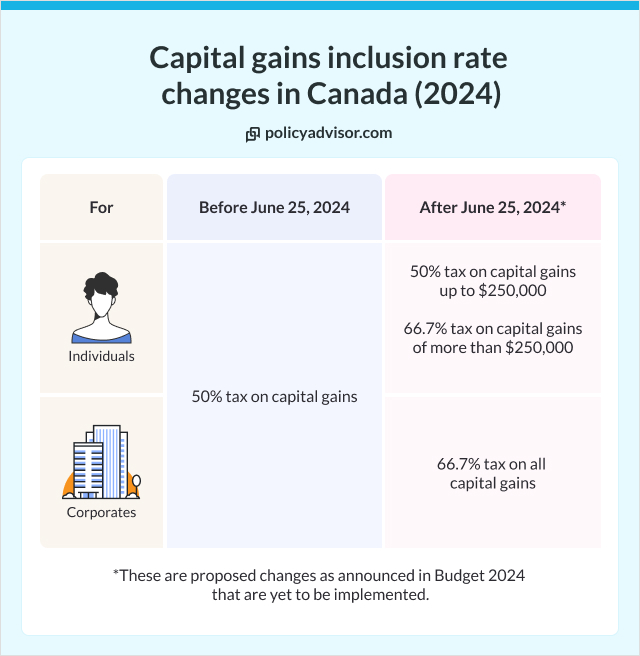

The Canadian government had proposed to increase the capital gains inclusion rate from 50 percent to 66.7 percent for any profits above $250,000.

The increased inclusion rate was to come into effect from June 25, 2024, but it has been deferred. On January 31, 2025, the Canadian government delayed the implementation of the increased inclusion rate indefinitely.

They have cited the need for further analysis to ensure the policy aligns with their vision of fairness and economic growth.

Although this delay might come as a relief for Canadians, the policy could be enacted later. Individuals and businesses with significant capital gains should remain prepared with long-term strategies.

How will the changes in capital gains taxation affect individuals?

Individual taxpayers would continue to pay tax on 50 percent of their capital gains up to $250,000 even after the proposed changes would come into effect. For any capital gains beyond $250,000, the individual will have to pay taxes according to the new rate of 66.7 percent. Here’s a breakdown of what will happen before and after the revised inclusion rate is approved and implemented:

Before increase in inclusion rate: The rules don’t change—as an individual taxpayer, you will pay tax on 50 percent of your capital gains of up to $250,000.

After increase in inclusion rate:

The new capital gains taxation rules will apply. While you will continue to pay tax on 50 percent of your capital gains of up to $250,000. Anything beyond that will be taxed at 66.7 percent.

Let’s understand with the help of an example.

John, an individual taxpayer, bought two assets worth $500,000 each in December 2022. He sold the former for $1,000,000 in January 2024 and he plans to sell the latter also for $1,000,000 in July 2024.

Period 1 (Capital gains realized before increase in inclusion rate)

For the first asset:

- John’s profit, or capital gain, is $500,000

- He will be required to pay taxes on 50 percent of the capital gain which is $250,000

Period 2 (Capital gains realized after increase in inclusion rate)

And for the second asset:

- His capital gain is also $500,000

- Should the proposed changes come into effect, he will have to pay taxes on 50 percent of the first $250,000 of capital gain i.e. on $125,000

- He will need to pay taxes on 66.7 percent of the remaining capital gain of $250,000 that is on $167,500

- So total amount of taxable income from the second sale will be $292,500

How will the changes in capital gains taxation affect corporations?

The proposed capital gains tax changes will increase the inclusion rate to 66.7 percent from 50 percent without a $250,000 limit for corporations. This means that regardless of the amount of profit on the sale of an asset, corporations will pay tax on two-thirds of their capital gains.

The new rules can affect corporations eligible for the Small Business Deduction. Currently, small businesses making under $500,000 of business income qualify for lower tax rates. However, if a company earns over $150,000 from investments, it can lose this tax advantage. If the Capital Gains Inclusion Rate (CGIR) rises, companies might reach this $150,000 limit faster, resulting in fewer or no tax breaks, causing concern for them.

How do the proposed capital gains tax changes affect individual homeowners?

Any real estate (apart from your primary or principal residence) that you sell after the new inclusion rate comes into effect, will fall under the proposed capital gains taxation. This means that any profit that you make beyond the designated $250,000 will be taxed at 66.7 percent inclusion rate.

To clarify, your principal residence, which is where you live for most of your life, is exempt from capital gains taxes. Regardless of how much you profit on the sale of your principal residence, you will not have to pay capital gains taxes on it.

How does the proposed capital gains tax affect estate plans?

Reviewing estate plans is important following the Budget 2024 because it didn’t clarify if there will be exceptions for capital gains upon death, as per the proposed changes. Currently, when a taxpayer dies, all their assets are considered sold at market value, leading to capital gains taxes. This is called deemed disposition.

With the proposed changes, these taxes on deemed disposition might also increase. Therefore, it’s advisable for individuals to reassess their estate plans considering the potential higher tax burden upon death.

What can you do to minimize losses due to these new rules?

While evading taxes is simply not an option and is a criminal offense, there are ways to legally pay the least amount of tax possible. These are:

- PPlan the sale of your assets before the revised inclusion rate is enforced to avoid the possibility of paying tax at the rate of 66.7 percent on your capital gains, should the proposed changes go through

- Hold your investments in a registered account such as the Registered Retirement Savings Plan (RRSP) or the Registered Education Savings Plan (RESP)

- Claim a capital loss to offset the capital gains. Since you don’t pay taxes on capital losses, you can use these to lower the amount of tax you owe on any capital gains. In fact, if your losses are more than your profits, you can use them to offset your capital gains for the past three years

- If you own real estate but don’t have a principal residence registered with the Canada Revenue Agency (CRA), you can do that and claim an exemption from capital gains taxes

Can life insurance help offset the increased inclusion rate with the proposed capital gains changes?

Absolutely! Permanent life insurance is a non-taxable way to build and generate wealth over time. With permanent life insurance, policyholders can pay more than just the premiums. The additional funds are invested and continue to grow over time and generate cash value.

Permanent life insurance policyholders also get additional benefits, including:

- Tax benefits for individuals: The cash value is tax-deferred—policyholders don’t need to pay taxes on the investment till they withdraw it

- Tax benefits for corporations: Business-owned permanent life insurance can help corporations avoid paying passive income tax rate, which in some cases can be as high as 50 percent. By investing in permanent life insurance policies, corporations can accumulate cash value on a tax-deferred basis, which can be accessed in the future to supplement income or fund business needs without triggering immediate tax liabilities

- Tax-free death benefit for individuals and corporations: The death benefit that beneficiaries receive is not taxable. If an appropriate amount of life insurance is purchased, it can also help cover the cost of the higher taxes

Life insurance and the proposed capital gains tax rate: An example

John and Emily own a primary residence and a rental property. Upon John’s passing his assets transfer to Emily. When Emily also passes away, the assets go to the children, but trigger a deemed disposition capital gains tax.

| Investment type | Current capital gains structure | Proposed changes |

| Primary residence value

(no tax liability) |

$1,000,000 | $1,000,000 |

| Rental property value | $600,000 | $600,000 |

| Capital gain on rental property (cost basis $100,000) | $500,000 | $500,000 |

| Taxable amount | $250,000

(50% of capital gains) |

$292,500

(50% of capital gains up to $250k and $66.7% of capital gains above $250k) |

| Tax liability

(50% tax rate) |

$125,000 | $146,250 |

In this scenario, without adequate estate planning, the children might face challenges to pay the increased tax liability, such as needing a bank loan or selling assets to pay taxes. Life insurance could provide a solution.

John and Emily could buy a life insurance policy with a death benefit equal to the projected tax-liability their children might incur upon inheriting the business. The new life insurance policy can provide the following benefits to the family:

- Liquidity: Life insurance could provide the necessary cash to cover the higher tax liability on the rental property, avoiding the need to sell the property

- Efficient tax settlement: By using the death benefit to settle the tax bill, John and Emily’s estate can preserve the rental property for the beneficiaries, maintaining its value within the estate

- Probate avoidance: Proceeds can be paid directly to the children, avoiding delays and expenses associated with probate, providing immediate financial relief

- Flexibility: Participating whole life insurance can be customized to cover a growing amount of the tax liability, providing precise financial protection for the estate

- Tax efficiency: The beneficiaries can receive the life insurance proceeds free from income tax, maximizing the value of the inheritance

- Peace of mind: By incorporating life insurance into the estate plan, John and Emily can ensure that their beneficiaries are financially protected and the estate distribution occurs smoothly, providing peace of mind for all involved

Read more about the tax implications of life insurance

We’re here to help!

We know all of this can sound overwhelming, so we’re here to help. Our expert and licensed advisors will help you understand the impact of the new capital gains taxations on your assets. Schedule a call with us today!

Frequently Asked Questions

Who is likely to be affected by the new capital gains inclusion rate?

The new capital gains inclusion rate is mostly going to affect active investors or corporations who realize capital gains on a regular basis through sales of assets. However, it will also affect individuals, business owners, homeowners, trusts, and corporations in those years where they have significant sales of assets, even if such sales happen occasionally for them.

What is the capital gains tax in Canada in 2024?

The inclusion rate—the amount of taxable capital gain—has been increased from 50 percent to 67 percent for capital gains above $250,000.

Can I gift a house to my children without paying capital gains tax?

While there is no gift tax in Canada, capital gains will have to be paid on the house you give to your children unless it is your principal residence.

Disclaimer: The information provided herein is for informational purposes only and should not in any way be construed as tax advice. You should consult with a qualified tax professional or financial expert regarding your specific tax situation and needs.

The Canadian government had proposed to increase the capital gains inclusion rate from 50 percent to 66.7 percent for any profits above $250,000. The increased inclusion rate was to come into effect from June 25, 2024, but as of January 31, 2025, the implementation of the increased inclusion rate has been deferred indefinitely, citing the need for further analysis to ensure the policy aligns with their vision of fairness and economic growth.