- Life insurance is a way for seniors to leave a tax-free sum of money to their loved ones or estate

- Term life insurance is not typically available for seniors past the age of 75

- Whole life insurance is a great option for seniors who either own businesses or are looking to protect their estate

- Seniors with health issues can still get coverage through guaranteed life insurance

Most people assume that life insurance for seniors is either not worth it or impossible to be approved, but that is not true. Even those aged 60 or over can take comfort in knowing they can still get life insurance coverage in Canada.

Read on to find out what your coverage options are and how you can secure the protection you need at retirement age.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Can seniors get life insurance in Canada?

Yes, seniors and older Canadian citizens can get life insurance in Canada. They can usually get it up to 70 or 80 years of age. Most insurers offer various options for older adults, such as term life, whole life, and guaranteed acceptance insurance policies.

Guaranteed acceptance plans typically require no medical exams, making them the perfect option for individuals with certain pre-existing health concerns. Term life insurance is more affordable and suitable for seniors who live on fixed incomes. Even though the premiums may be higher for seniors due to their age, coverage is usually not denied, even for individuals over 75; however, you should always review each insurer’s underwriting guidelines.

Which are the best life insurance companies for seniors in Canada?

Some of the best life insurance companies for seniors in Canada include Canada Life, Wawanesa, Industrial Alliance (iA), and Canada Protection Plan. Take a deep dive into their offerings and ratings:

| Company | Key features | Best for | Rating (Out of 5) |

| Canada Life | Short 5-year term option, ideal for elderly individuals aged 80-85 | Elderly individuals (ages 80-85) | 4/5 |

| Wawanesa | Offers lower rates by using your actual age instead of your nearest birthday | Individuals seeking lower premiums | 4/5 |

| Industrial Alliance (iA) | Popular for guaranteed life insurance plans, with approval up to age 80 | Those needing guaranteed coverage up to age 80 | 4/5 |

| Canada Protection Plan (CPP) | Known for guaranteed life insurance with no health questions required for approval | Individuals with health concerns or pre-existing conditions | 4/5 |

Why do seniors need life insurance?

Seniors need life insurance to give their family financial security and peace of mind, pay off mortgage and outstanding debt, cover medical debt, support dependents, or leave a charitable legacy. Through life insurance, individuals can plan ahead for their retirement and create a financial net for their loved ones.

- To pay off the mortgage: Not every Canadian has paid off their mortgage by the time they have reached their 50s or 60s. A death benefit payout from the insurance policy would enable surviving loved ones to handle it

- To pay off any outstanding debts: Similarly, beneficiaries can use the payment to cover any other leftover debt such as credit card bills, personal or business loans, and more

- To cover funeral arrangement expenses: Life insurance can also give surviving loved ones the space to grieve without worrying about how they can afford to pay for burial costs

- To cover medical debt: Some life policies come with benefits you can use now, to help pay for costs like long-term care and prescriptions, or to give an advance on the payout in the event of a terminal illness

- To provide for a surviving spouse: Life insurance can help a surviving spouse maintain their same standard of living and keep up with daily expenses and bills

- To provide for dependents: Seniors who take care of family members with special needs can make sure the money from their life insurance is used to keep providing for those loved ones

- To supplement retirement savings: Many older Canadians use the money they get from a whole life policy’s cash value to supplement their pension and help give them some extra cash

- To leave an inheritance for children and grandchildren: Life insurance is a fantastic estate planning tool that helps seniors leave money behind for children, grandchildren, and other family members

- To leave a legacy for a charity of choice: Similarly, life coverage gives seniors a way to leave a gift behind for a charity or cause they care deeply about

- To ensure protection: In Canada, there is no government life insurance for seniors. Any older people who want this kind of protection must buy it themselves

What types of life insurance can seniors get in Canada?

Depending on their individual health and coverage needs, seniors may choose from traditionally underwritten life insurance or no-medical life insurance policies. Take a look at these options in detail:

1. Traditionally underwritten life insurance

Traditional policies are fully underwritten, which means applicants have to answer a lot of questions about their health history. They may also have to take a medical exam. Traditionally underwritten life insurance comes in two types:

- Term life insurance

- Whole life insurance

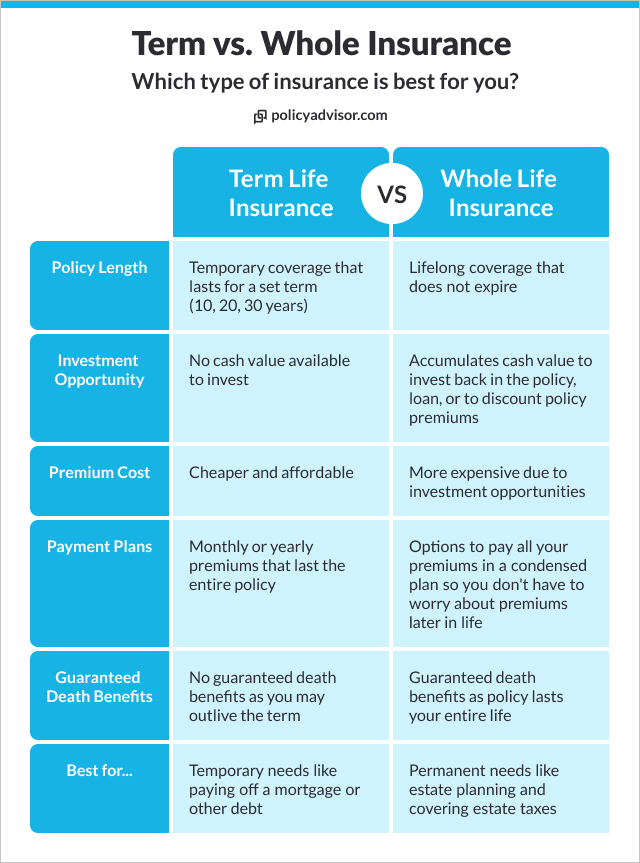

Term life insurance for seniors

Term life insurance policies cover you for a specific length of time, called a term. It pays a tax-free, lump-sum payment called a death benefit to your beneficiaries if you die within the term.

A healthy 60-year-old who needs life insurance for a temporary need like paying off their mortgage will find that a term policy is the best choice. It’s the most affordable type of policy and can take care of their needs.

Whole life insurance for seniors

Whole life insurance is a type of permanent insurance that covers you for your entire life. It is best for final expenses like funeral costs, outstanding debts, and end-of-life medical costs. It also has the living benefit of a cash value component. This cash value may be accessed during your lifetime either by withdrawing or borrowing against it.

Whole life policies are generally more expensive than term. It is also just one type of permanent insurance policy, aside from universal life insurance and term-to-100.

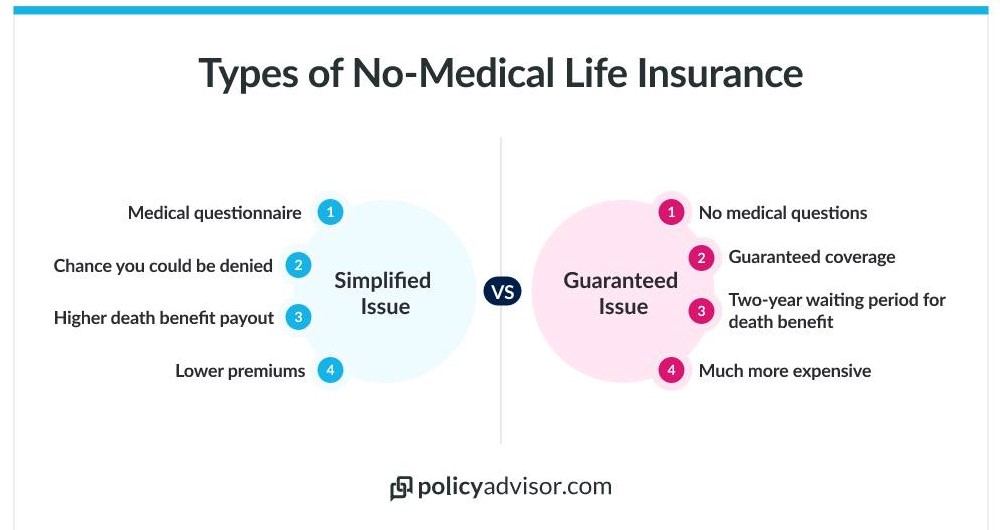

2. No-medical life insurance

No medical life policies have very few medical questions and do not require a medical exam. No medical insurance has two types: simplified issue life insurance and guaranteed issue life insurance. They are best for people who:

- Have an underlying health condition or medical issue

- Have hobbies or pastimes that are considered dangerous (like skydiving)

- Need to get coverage quickly

Simplified life insurance for seniors

Simplified issue life insurance asks you a few questions about your medical history when you apply, instead of a full exam. However, they tend to be more expensive and usually have limitations like:

- A lower death benefit

- Can have a waiting period of 1-2 years before coverage starts

Guaranteed life insurance for seniors

Guaranteed life insurance has NO health questions at all, so you’re guaranteed to get approved. But it comes with a lot of limitations, like:

- Maximum death benefit amount of $50,000

- Almost always has a waiting period of 1-2 years before coverage starts

This is a last-resort insurance plan. It’s there for those who aren’t able to get traditional life insurance policies or simplified issue policies.

Learn more about the different types of life insurance in Canada.

Which is better for seniors, whole life or term life insurance?

Both term and whole life insurance offer distinct advantages for seniors. Term life insurance provides affordable coverage for final expenses and outstanding debts. However, premiums increase significantly after age 60 and can be difficult to sustain.

Whole life insurance while initially more expensive, can help secure your legacy by covering estate taxes and leaving an inheritance for your loved ones. That said, it takes time for a whole life policy to accumulate sufficient value, making it more suitable for seniors who either own businesses or are looking to protect their estate.

What riders and additional benefits are available on life insurance for seniors?

Life insurance for seniors offers several riders or add-ons that can enhance its coverage. Some of them are:

- Accidental death benefit: This add-on multiplies the basic coverage amount if the insured dies in an accident

- Terminal illness benefit: This benefit allows the insured to access 50-75% of their death benefit if they’re diagnosed with a terminal illness

- Disability credit insurance: This add-on covers the insured’s financial obligations if they become disabled

- Waiver of premiums: This add-on cancels future premium payments if the insured becomes completely disabled before the age of 60 and the disability lasts longer than 6 months

Note that the availability of these options depends on your policy type and insurer, which is why we recommend you speak to a licensed insurance advisor to understand your coverage options better.

How much does life insurance for elderly people in Canada cost?

It depends on factors like age, type of policy, and more. Life insurance for seniors over 65 can be anywhere from $55 to over $100 a month for term life insurance. Or, life insurance for seniors 65 and over can be around $100 to start.

Life insurance costs for seniors over 50 in Canada

For those in their 50s, life insurance tends to be more affordable and accessible, ranging between $50 and $170 per month. Policies can be structured to offer a balance of coverage and cost, with the potential for both term and whole life insurance options.

| Policy Type | Cost (Approx.) |

| 10-year term | $35/month |

| 20-year term | $61/month |

| Whole life | $111/month |

| Term-to-100 | $179/month |

Life insurance costs for seniors over 60 in Canada

Seniors over 60 see an increase in premiums due to age-related health risks. Policy prices can range from $50 to $240 per month. There is a wider range of policy options available, including term, whole life, and term-to-100 policies.

| Policy Type | Cost (Approx.) |

| 10-year term | $55/month |

| 20-year term | $108/month |

| Whole life | $149/month |

| Term-to-100 | $241/month |

Life insurance costs for seniors over 70 in Canada

For those in their 70s, premiums are higher, reflecting increased health risks. Life insurance policies can range between $90 to $320 per month for individuals in their 70s. Policies like term-to-100 are designed to provide lifetime coverage, albeit at a higher cost.

| Policy type | Cost (Approx.) |

| 10-year term | $94/month |

| 20-year term | N/A |

| Whole life | $99/month |

| Term-to-100 | $313/month |

Life insurance costs for seniors over 80 in Canada

Life insurance options for those over 80 are limited and come with high premiums, typically ranging between $200 to $450, due to the higher mortality risk. Policies mainly focus on final expense coverage rather than extensive financial planning.

| Policy type | Cost (Approx.) |

| 10-year term | $205/month |

| 20-year term | N/A |

| Whole life | $131/month |

| Term-to-100 | $441/month |

*Quote for $100,000 in life insurance coverage for a non-smoking female resident of Ontario in good health. 20-year coverage not available past age 65.

What affects the cost of life insurance for older adults?

For seniors, just like for everyone, the cost of life insurance premiums depends on factors such as their age, health history, smoking status, sex and the type of policy that they have purchased.

- Age: The older you are, the higher the premiums due to increased health risks and shorter life expectancy

- Health status: Current health and medical history heavily influence premiums; chronic conditions can lead to higher costs or denial of coverage

- Type of policy: Term life insurance generally costs less than permanent policies like whole life, which offer lifelong coverage and additional benefits

- Smoking status: Smokers pay significantly more for life insurance due to the increased health risks associated with tobacco use

- Gender: Women typically pay lower premiums than men because they have a longer life expectancy

- Coverage amount: Higher death benefits mean higher premiums, as larger coverage amounts represent a greater financial risk for the insurer

Health is a major contributing factor for seniors especially, just because our health generally declines the older we get. Age and health are two of the biggest factors that will affect your cost, and whether you can get coverage at all as a senior.

What is the most affordable type of Canadian life insurance for seniors?

Term life insurance is the cheapest type of life insurance for seniors and for Canadians in general. Be aware that seniors have limited options for term insurance, depending on their age. Depending on your needs, it may not be the best option for you.

Is senior life insurance in Canada worth it?

Yes. Life insurance for seniors provides financial protection for your loved ones by covering your outstanding debts, mortgages, and final expenses like funeral costs after you pass away.

In addition to this, senior life insurance offers several benefits, such as:

- Estate protection: Whole life insurance prevents your legacy assets from being sold off prematurely. With a guaranteed death benefit, it ensures that your beneficiaries have the financial assistance they need to cover estate taxes

- Leaving an inheritance: Life insurance offers a tax-efficient way to pass down wealth to children and grandchildren. For example, you can allocate funds specifically for their education

- Supporting a cause: You can create a lasting impact by designating a portion of your life insurance benefit to charities you care about

When is it a good time to get life insurance for seniors?

The best time to get life insurance for seniors is while you:

a) Still meet the age and health requirements: Leading insurers, such as Canada Life, offer coverage up to age 85. However, premiums increase with age, so the earlier you secure coverage, the better. Additionally, while many insurers do cover pre-existing conditions, applying for a policy when you are in good health typically results in lower premiums and fewer restrictions

b) Have outstanding debts: If you have a mortgage, loans, or other debts that could burden your family after your passing, consider getting coverage sooner rather than later

c) Want to plan ahead: If you wish to cover your funeral expenses or leave a legacy for your loved ones, you may want to lock in coverage while you still have more options

Is a senior’s life insurance policy a costly mistake?

No. Let’s look at the actual costs: term life insurance for people in their 50s typically costs $35/month for a 10-year term and $61/month for a 20-year term. Permanent plans for the same age group cost around $111/month.

When you consider how the death benefit can be used, paying off debts, covering final expenses, and protecting your estate, life insurance becomes a valuable investment rather than a costly mistake.

How to buy life insurance for seniors in Canada?

Seniors can easily buy life insurance in Canada once they have figured out their needs. You can also look at policy marketplaces and apply via your phone to get the best rates. For a more customized experience, you can connect with our experts at PolicyAdvisor.

1. Figure out your needs

Start by thinking through your reason for buying life insurance and what you need to secure. This will help you determine what kind of coverage you need.

If you’re not sure, try out our free life insurance calculator. It will help you decide. You can also contact one of our licensed insurance advisors for one-on-one help.

2. Get free life insurance quotes for seniors from PolicyAdvisor

Once you’ve decided what kind of policy and how much coverage you need, you can compare the lowest insurance quotes for seniors online. Our quoting tool searches the Canadian insurance market for you in seconds.

This lets you easily compare quotes from more than 30 of the best life insurance companies for seniors in seconds.

3. Apply online or over the phone

Select the quote you want and submit your application online by answering some personal questions. You can also contact us and let our agents go through the process with you, saving you time and money.

Frequently asked questions

What is the best life insurance for older people in Canada?

The best type of life insurance for seniors depends on their financial goals and obligations. Here’s what each type has to offer:

- Term life insurance: While it covers you for a limited period (typically 10, 20, or 30 years), term life insurance helps you pay off debts and cover funeral expenses. It also allows you to tailor your coverage (specifically policy duration) to meet specific financial protection goals

- Whole life insurance: This type of policy protects you for your entire life while building cash value you can access during your lifetime. For seniors, it’s particularly valuable for estate protection, preserving an inheritance, leaving a legacy, and covering final expenses

- Guaranteed life insurance: Designed for those who may not qualify for traditional life insurance, this option requires no medical underwriting. It ensures financial protection for your family and covers outstanding debts upon your passing

To ensure you select the right coverage for you and your loved ones, we recommend you book a free consultation with our licensed advisors who can guide you through different options.

Should a 70 year old have life insurance?

Yes. A 70-year-old with outstanding financial obligations should strongly consider life insurance. Not only will it help protect their loved ones from any financial burdens after their passing, but also help cover their final expenses and leave a legacy for family members or charitable causes.

How much life insurance do seniors need?

Normally, experts say you should get 10-15x your annual income in coverage. Canadian life insurance for seniors is different; many are already retired and only want to help pay for final expenses or leave an inheritance for their family.

How do pre-existing conditions affect life insurance for older people?

Pre-existing conditions affect:

- What kind of life insurance you can get

- Whether you will be approved for coverage

- How much your life insurance rates will be

Many seniors in Canada already have health issues like cancer, high blood pressure, diabetes, and more. These are all considered pre-existing health issues that will affect their insurance options.

However, there are still options for seniors with health issues to obtain coverage through no-medical policies. Seniors can still get insurance coverage even if they have bad health and even without taking a medical exam.

Can seniors convert or renew their life insurance policy?

While most term life policies can be renewed or converted into a permanent policy at the end of the term, not every senior may have these options. In general, most Canadian insurers will only let seniors renew or convert up until age 70 to 75.

What happens if my application is denied?

If your senior life insurance application is denied, you should contact our licensed insurance agents to help discuss how to move forward. We can help you take a look at why you may have been denied and see what the alternative options are.

What are the drawbacks of life insurance for older people?

The main downsides of life insurance are:

- Rates for seniors can be costly because of their age and health

- You may not be able to qualify for all types of life insurance policy

- Coverage amounts may be limited

- If you don’t use your cash value before you pass away, you will lose it

Is life insurance for seniors different from other types of insurance?

Life insurance for seniors tends to be more expensive and can have less coverage than other types of insurance. Because of their advanced age and likely health issues, their policies cost more. And because most seniors are only focused on end-of-life expenses, they may not need as much coverage as a 30-year-old with a mortgage and two young kids.

What age is considered a senior for life insurance in Canada?

Typically, people who are 50 years old and over are seen as seniors in the life insurance industry in Canada.

Can I buy a life insurance policy for my senior parents?

Yes. You can get a life insurance policy for your parents. You just need to meet requirements like:

- Consent — They have to be aware that you are taking out a policy on them

- Age restrictions — They have to be within the eligible age range, so you can’t apply for them just because they are 90 and you are younger

- Insurable interest — You have to prove that if they pass away, you would be affected financially

- Personal details — You will need to submit information like their health and financial details

Is there government life insurance for seniors?

No. There is no government life insurance for seniors in Canada like there are programs for health insurance. To get coverage, a senior must purchase life insurance privately. To find an affordable life insurance option for your financial goals, contact an advisor today!

Life insurance is beneficial for any senior who wishes to leave tax-free money for their loved ones or estate. There are many term life insurance options available up to age 75. Permanent life insurance is a great option to cover funeral expenses and medical bills. Seniors with poor health can still qualify for life insurance coverage if they apply for no-medical plans that don’t ask for a medical exam.