1-888-601-9980

1-888-601-9980The Best

Life Insurance

in Manitoba

Get a life insurance quote in Manitoba within minutes!

Types of life insurance in Manitoba

Buying life insurance in Manitoba can be tricky, as life insurance is not a one-size-fits-all product. Different categories of life insurance policies can be offered to individuals based on their age, gender, medical history, lifestyle, etc.

Term life insurance

Term life insurance in Manitoba is an affordable and straightforward insurance option that provides coverage for a specific period, usually between 10 and 30 years. This type of insurance is ideal for individuals seeking temporary coverage during key life stages, such as raising a family or paying off a mortgage.

Whole life insurance

Whole life insurance in Manitoba is a permanent life insurance policy that provides lifelong coverage as long as premiums are paid. It includes a cash value component that grows over time, which policyholders can borrow against or withdraw.

This type of insurance is ideal for those looking for long-term financial security and wealth-building opportunities and is preferred by many Canadians as an all-purpose financial solution.

Other types of insurance in Manitoba

Disability insurance

As of 2019, about 175,000 people in Manitoba, Canada, or roughly one in six people, have some degree of disability.

Disability insurance in Manitoba provides financial protection by replacing a portion of your income if you become unable to work due to illness or injury.

This insurance helps cover essential expenses, such as mortgage payments, utilities, and daily living costs, ensuring financial stability during recovery.

Critical illness insurance

In Canada, 31% of males and 23% of females are expected to develop a critical illness by the time they reach 61 years of age.

Critical illness insurance in Manitoba offers financial support by providing a lump-sum payment if you’re diagnosed with a covered serious illness, such as cancer, heart attack, or stroke.

This benefit helps cover medical expenses, lost income, or other financial needs during recovery, allowing you to focus on your health.

Health insurance

Manitoba has a population of approximately 1.3 million people, with about 57% residing in the urban center of Winnipeg.

Private health insurance in Manitoba supplements the province’s public healthcare system by covering additional medical costs not included in provincial health plans. This can include prescription drugs, dental care, vision care, and extended health services like physiotherapy or massage therapy.

Visitor insurance

Visitor insurance in Manitoba provides essential coverage for unexpected events while traveling, including medical emergencies, trip cancellations, lost luggage, and flight delays.

Given that provincial health coverage is limited outside of Canada, travel insurance ensures you’re protected from significant financial risks abroad.

How much does life insurance cost in Manitoba?

Life insurance premiums vary widely from company to company. However, there are some ballpark average values that can help to determine the cost of life insurance in Manitoba. Take a look:

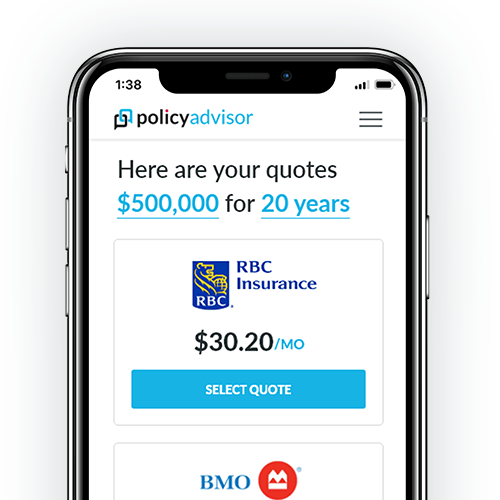

- A 20-year term life insurance in Manitoba with approximately $500,000 coverage value may cost around $890/year for a 35-year-old, smoking male

- Whole life insurance in Manitoba for a $300,000 coverage amount may cost around $2,978/year for a 45-year-old, non-smoking female

- Universal life insurance in Manitoba for a $600,000 coverage amount will cost around $4,456/year for a 40-year-old, non-smoking female

The values may vary slightly depending on the individual’s insurability risks. People with high-risk jobs and compromising lifestyles end up paying higher premiums than healthy individuals.

How much life insurance do you need in Manitoba?

With the rising cost of living in Manitoba, you need to make sure you have enough insurance to cover your future needs. You want enough insurance to cover your family’s living expenses in Manitoba as well as outstanding debt repayment.

Generally speaking, you should select a death benefit that offers a minimum of 10 times your yearly income. But, for a more precise estimate, take into account your debts, the cost of living for your family, the future educational expenses of your children, final expenses, and any other financial objectives, like charitable contributions.

Our knowledgeable insurance advisors work with you to determine the appropriate level of life insurance coverage in Manitoba, taking into account both your personal preferences and financial status.

Our calculator quickly determines what you need and gives you the best options

Best life insurance companies in Manitoba

Some of the top life insurance companies in Manitoba include:

Best for affordability: BMO Insurance

Best for financial strength: Canada Life

Best for non-medical: Canada Protection Plan

Best for stability: Desjardins

Best for personalization: Empire Life

Best for families: Equitable Life

Best for digital innovation: Manulife

Best for value for money: RBC

Best for buying in-person: Sun Life

Best for Marijuana Users: Beneva

Best for Smokers: iA Financial Group

Explore life insurance quotes in other provinces

Get life insurance quotes in different cities

No-medical life insurance

Many people in Manitoba live with medical conditions and health issues they assume will prevent them from getting insurance coverage. Others need insurance coverage more quickly than it takes to get approved through traditional medical underwriting . Fortunately, Manitobans can get an insurance policy without a medical examination or bloodwork.

Given our recent global pandemic and a greater focus on physical distancing, many Canadians are uncomfortable with the thought of going to a busy doctor’s office for medical tests or inviting a stranger into their home for a paramedical exam.

PolicyAdvisor offers several ways for those in Manitoba to apply for life insurance without a face-to-face meeting. Besides an aversion for blood tests or prior health concerns, there are many reasons someone might elect for non-medical life insurance. In these cases, a simplified or guaranteed issue insurance policy gives a applicant more options.

You can shop for quotes, speak to a licensed Manitoba online insurance broker, and apply for life insurance all without leaving your own home or having to meet face-to-face.

Why PolicyAdvisor?

PolicyAdvisor makes finding life insurance simple. Compare quotes, get expert advice, and find the best policy for your needs—all in one place.

- Save time: Get instant quotes from Manitoba’s top life insurance companies

- Save money: Compare multiple quotes to find the best price

- Shop anywhere: Use our online tools to compare quotes from your phone or computer

- Personalized service: Receive expert advice from a dedicated insurance advisor

Frequently asked questions

Are life insurance premiums in Manitoba tax-deductible?

Life insurance premiums in Manitoba are generally not tax-deductible for individuals. However, if a business owns a life insurance policy on an employee or key person, the premiums may be deductible under specific circumstances.

To understand the tax implications of your life insurance policy, it’s best to consult with an insurance advisor (such as our experts at PolicyAdvisor).

Can I purchase life insurance in Manitoba if I have a pre-existing medical condition?

Yes, you can still purchase life insurance in Manitoba if you have a pre-existing medical condition. However, the availability and cost of coverage may be affected.

Some insurers may offer coverage at a higher premium or exclude certain conditions, while others might provide guaranteed issue policies with no medical exam, though at a higher cost and with lower coverage limits. To get the best rates at an affordable price, consult with expert life insurance brokers in Manitoba.

What happens if I miss a premium payment on my life insurance policy?

If you miss a premium payment on your life insurance policy in Manitoba, most policies have a grace period, typically 30 days, during which you can make the payment without losing coverage.

If the premium isn’t paid within this period, the policy may lapse, and coverage will end. Some policies offer reinstatement options, but this may require a new medical exam and payment of overdue premiums.

Can I change my life insurance policy in Manitoba if my needs change?

Yes, many life insurance policies in Manitoba offer flexibility. For example, you can often convert a term life insurance policy to a whole life policy without a medical exam or adjust the coverage amount if your financial situation changes.

It’s important to review your policy regularly and discuss any changes with your life insurance broker or advisor to ensure it continues to meet your needs.