1-888-601-9980

1-888-601-9980

- Term life insurance is a temporary protection meant to cover an insured person (or their dependents) financial risk should something happen to them.

- Renewing or converting an existing term life insurance policy can be expensive, but may be one's only choice for coverage if they have accrued any health issues during their coverage period.

- One can save money by applying for life insurance again rather than renewing their policy.

Most term life insurance policies come with an expiry date, upon which the policy matures and your coverage ends. Generally, one can only own a term policy for a set period time; which can last anywhere between 5 and 30 years depending on your policy. While the policy is in force, you must pay a monthly premium to guarantee the death benefit to your beneficiaries if you die.

But people don’t purchase term life insurance policies in the hopes of a big payout. The entire point is to provide a financial safety net for your loved ones to fall back on if you happen to pass away unexpectedly.

So what happens if you outlive your policy? What if your plan expires while you’re still alive and kicking?

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

A term life insurance policy is usually bought only for short term obligation – to provide for dependents until they start earning and pay off pending loans and mortgages. It’s possible you won’t need the insurance coverage once your term period is up.

But this doesn’t always apply to everyone’s situation. People often end up requiring extended insurance coverage due to unforeseen circumstances. Fortunately, for those who need life insurance upon the expiration of their initial term policy, there are multiple options.

What to do when your term life insurance expires

As we mentioned, people sign up for a term life insurance policy with the hope that they never need to use it. But many feel it is a necessary investment to make to keep your family’s financial future secure. This same frame of mind is required when exploring your options when your coverage has ended.

You need to assess your latest financial situation. Do you still have dependents? Is your estate sufficient enough to sustain them into adulthood? Is your mortgage still pending? Does your partner depend on your income to main their quality of life? Only an honest introspection into your finances can help you understand these future needs.

If you determine that you’ll need continued coverage then broach this conversation with your insurance advisor or broker 6 months before the maturity date. Any later and you risk getting caught in a coverage gap. This gives you enough time to study all the available options and choose the one that is best for you.

What if I decide against life insurance coverage if I outlive my current policy?

If you’re fortunate enough to not require any more insurance coverage, then all you need to do is pay the last premium and wait out the policy. Once the plan ends, you won’t be covered and nor will your beneficiaries receive any payout upon your death. Of course, that means you no longer need to pay your monthly premium as well.

If your children are well on their way to providing for themselves, you’re completely debt-free, and your partner is capable of maintaining their expenses without your income it doesn’t make much sense to continue paying for a term policy you may not need.

But letting your coverage lapse entirely is not the advised course of action for most policyholders if you still have obligations – including those listed above – and have not saved up the cash to cover them at that time.

What do I do if I still need life insurance after the expiry of my term?

Over the years, your net worth might have risen or you may have fewer financial obligations. In many cases, your coverage requirements will have changed from the time you bought your first term policy.

Doing a financial assessment with a life insurance needs calculator is an important step in understanding your pending coverage needs.

If you find you’re still in the market for life insurance once your policy ends then you have 3 options.

- Renew your term with your current insurance provider.

- Convert your current policy into whole life insurance.

- Buy a completely new term life insurance policy.

Below is a detailed explanation of each option with its pros and cons to help you make the right choice.

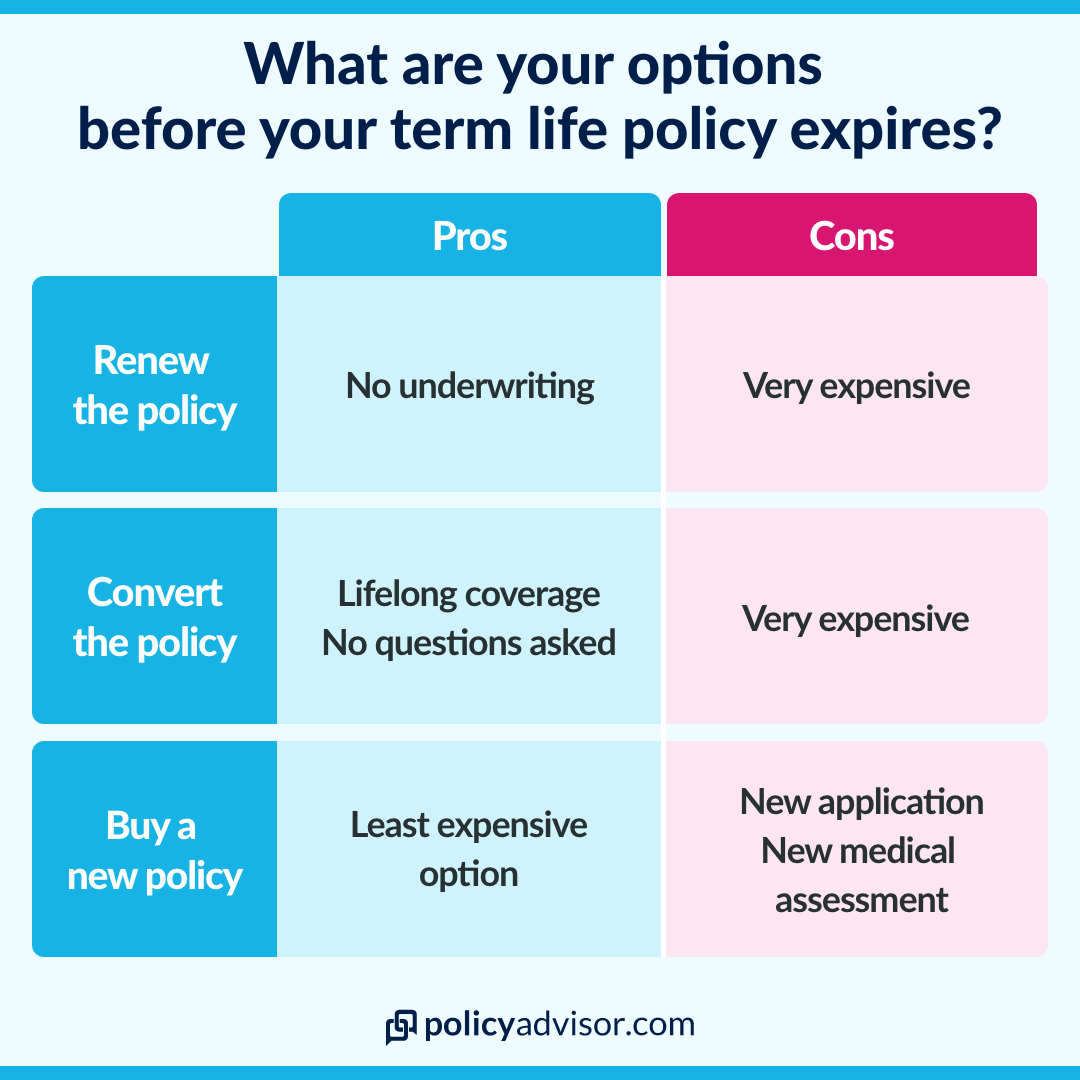

Renew current term life insurance

Many term life insurance companies offer the choice to extend the policy term beyond the initially agreed date. This is referred to as a renewability rider and may have been touted as a feature of your policy when you first purchased it. This extension is usually valid until you reach a certain age (generally 75 years), though it varies from company to company.

How do I renew my term life insurance policy?

If you like your current coverage and don’t mind paying more expensive premiums, then renewing your term life insurance policy is an easy choice.

You are saved from the hassle of shopping for a new policy and you don’t need to spend time researching and discussing with your loved ones about a new term policy. All that is required of you is to continue paying the newly set premiums.

Another positive part of a renewable policy is that you’re exempt from displaying proof of insurability. Simply put, you won’t need to undergo an extensive medical exam to qualify for the insurance policy again. This is ideal for those who have experienced drastic declines in health during the term of the first policy. Having a permanent medical condition or just generally poor health is seen as a potential risk by most leading insurance companies that can possibly disqualify you from purchasing a new policy.

As mentioned, the benefits of renewing a policy come at a much higher cost. The revised premium to be paid with a policy renewal can be 5-10 times more expensive than your previous coverage. This is to cover the lack of proof of insurability. The insurance provider has no way of knowing how healthy you are without a medical examination. There is an assumption that your health deteriorates during the previous term.

If you’re in relatively good health with no long term medical issues, then you should consider foregoing renewal. Instead, you could opt for a brand new policy which we’ll explain later.

Convert current term life insurance into permanent life insurance

Convertibility is another rider that some insurance companies offer as part of a base term life insurance policy. Once the term is up, you have the choice to convert your term policy into a whole life insurance plan.

The biggest difference between term life and whole life insurance is the added cash value it brings. Whole life insurance can be treated like an investment or financial vehicle to reduce your tax burden. All the cash that you put into your converted whole life insurance coverage accrues value over time and provides a guaranteed death benefit for your entire life.

How do I convert my term life insurance policy to permanent coverage?

If you choose to convert your policy, you will not only retain your coverage but also provide your beneficiaries with a large death benefit after you pass.

As with renewability, this rider does not require proof of insurability. No medical examinations, check-ups, or intrusive questions are asked. This policy is perfect for those with permanent medical conditions or diseases which prevent them from qualifying for a new policy.

But – similar to renewability – with these benefits come higher premiums. You can expect your premiums to go up substantially when you convert to whole life insurance.

Another possible downside is that converted policies are only eligible for selected permanent policies. That means you might not get to choose a specific policy provided by the company. Instead, your range of choices is limited to the ones the company included in your rider.

Another way to lower the premiums when converting to a whole life policy is by reducing your death benefit. If you feel a lower coverage will suit your needs just as well, then you can select a partial conversion wherein you retain some form of coverage with lower premiums.

Choosing to convert your term life insurance policy into a permanent policy can be the best alternative if your health has worsened during your initial term. But if your financial situation has dramatically altered, then a brand new policy with coverage that suits your new requirements may suit you better.

Buy a brand new life insurance policy

Only you can decide whether buying a brand new insurance policy is the right decision. If your financial needs have stayed level or increased, then considering a new policy with the right amount of coverage can be a smart option.

As with other choices, discuss your insurance needs with an experienced insurance advisor well before your policy expiry date. They can help you determine whether applying for new coverage is financially prudent. Even if you are rejected by an insurance provider for health-related reasons, the buffer time can be used to apply for a renewal with your current provider.

How do I buy a brand new life insurance policy?

Shopping for a new policy requires work. But there are many advantages to choosing new coverage.

Firstly, there are several types of policies available to choose from such as a term life insurance, no medical and guaranteed policies, whole life insurance, and universal life insurance among many others. When renewing or converting existing coverage you are limited to the types of policies and coverage your current provider offers.

Secondly, if you are in relatively good health, applying for fully medically underwritten coverage will generally have a much lower monthly premium compared to similar coverage that was renewed or converted. Because the insurance provider is setting the rates based on your health, you no longer have to pay for the risk involved in their uncertainty about your health.

Lastly, you can get as much or little coverage as you need at this time. Instead of being bound by the coverage amounts that are tied to your previous coverage you can take on a smaller policy to save money, or get more coverage for new obligations in your life (such as a new home or taking care of children or grandchildren).

Weighing your insurance options

Outliving your term life insurance can be considered good news. We want to live for as long as comfortably possible.

But it also brings forth the dilemma of considering whether to forego life insurance or not. If your dependents are now self-sufficient and your own retirement plans are in place, then you can simply let your policy expire upon maturity.

But if this is not the case, you need to consider new coverage. The best option for a relatively healthy person is buying a brand new policy to keep the cost of premiums as low as possible. If a medical condition makes a new policy difficult or unaffordable, then take advantage of the guaranteed riders in your initial policy. Most importantly, speak with an experienced insurance advisor to explore all your option and see where you can save money while maintaining the coverage you need.

A term life insurance policy comes with an expiration date. A policy typically lasts between 5 to 30 years and renews at that time at a higher premium. In cases where policyholders outlive their policy, their options include renewing their policy, choosing to forego life insurance and cancelling their policy, finding new coverage at a lower premium, or converting their coverage to whole life insurance policy.