1-888-601-9980

1-888-601-9980

- A beneficiary is an individual or organization who will receive your life insurance policy’s death benefit

- A revocable beneficiary can be changed at any time without the permission of that individual

- An irrevocable beneficiary cannot be changed without written permission of that individual

- Irrevocable beneficiaries also must sign off on any policy changes

Buying life insurance involves numerous questions and decisions. A life insurance application asks typical questions about your health and lifestyle, but there are some out-of-the-ordinary queries as well. Namely, you’ll need to decide who to designate as your beneficiaries and whether they’ll be revocable or irrevocable.

Sometimes, insurance policy language isn’t the most straightforward, which can make answering these questions more tricky than they have to be. Life insurance applicants might not even know the difference between a revocable or irrevocable beneficiary. But PolicyAdvisor is here to help make the insurance application jargon-free!

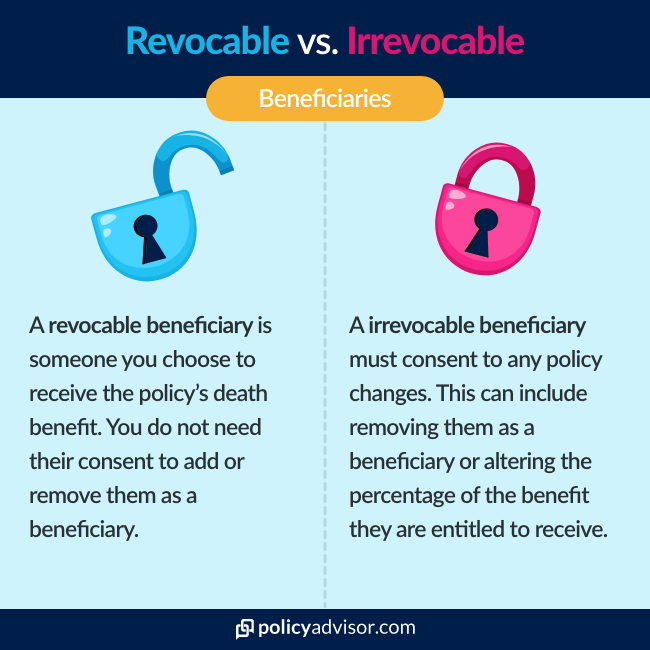

In the simplest terms, a beneficiary is a person who will get your life insurance payout. They can be a revocable or irrevocable beneficiary. The insurance company will require an irrevocable beneficiary’s signature and consent before making any change to your policy. In contrast, you won’t need a revocable beneficiary’s permission to make the same changes.

Policies generally default your beneficiaries to revocable, but there are particular reasons to make someone an irrevocable beneficiary. So, beyond those simple definitions, this article dives into detail about how to choose between the two types of beneficiaries for your life insurance policy.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is a life insurance beneficiary?

Generally, a beneficiary describes someone who receives something like money or property. A life insurance beneficiary can be a person, multiple people, or an organization that receives your insurance policy death benefit. You will be asked to name a beneficiary, regardless of the type of life insurance you’re applying for.

It’s common to designate a spouse or child as a beneficiary. They ultimately receive the life insurance proceeds as a tax-free, lump-sum cash payment to use for debts, living expenses, estate taxes, and funeral arrangements. This way, you leave your loved ones in a healthy financial position if you pass away.

Minor children can be life insurance beneficiaries. However, provincial laws commonly require children under 18 to receive payouts through an irrevocable trust until they reach the age of majority. The trustee can manage the funds on behalf of the minor child through the trust until they are legally able to hold that money themselves.

A policy owner may designate a charitable organization as their beneficiary as a last good deed. You may even select your business as a beneficiary — a typical corporate planning tactic in strategies like key person insurance or buy-sell agreements.

Your estate becomes the beneficiary if you don’t designate one. As a result, creditors can access your death benefit, and the money is subject to any applicable taxes, such as an estate administration tax. The remainder is divided based on your will or provincial intestacy laws. Therefore, if you want your death benefit to serve as a gift to a specific person or organization, it’s best to name them as a beneficiary, so they get to enjoy the full life insurance benefit.

What is an irrevocable beneficiary?

An irrevocable beneficiary is a beneficiary that must consent to any changes you request on your life insurance policy. Ultimately, irrevocable beneficiaries have a more substantial right to your death benefit because you can’t alter or cancel your life insurance without their permission.

Is an irrevocable beneficiary the primary beneficiary?

Primary beneficiaries are first in line to receive a policy’s death benefit. If your primary life insurance beneficiary is no longer alive when you die, the life insurance payout goes to your secondary or tertiary beneficiaries instead.

An irrevocable beneficiary is pretty much always your primary beneficiary. It’s rare for a secondary or tertiary beneficiary to be irrevocable.

Why would you want an irrevocable beneficiary?

Irrevocable beneficiary status ensures money goes to where you originally planned. It’s commonly used in divorce settlements or separation agreements, where each spouse lists their ex as an irrevocable beneficiary.

Suppose after a divorce, one spouse passes away. Their death means the other spouse no longer receives spousal or child aid payments for their dependent children. However, life insurance funds provide financial protection by making up for this loss.

An irrevocable beneficiary designation prevents a former spouse from changing the policy’s designation without the other person’s knowledge. Otherwise, some may attempt to remove their ex from their policy due to any number of circumstances.

Irrevocable beneficiary designations are also required when using a life insurance policy as loan collateral. The lender, such as a bank, would become the irrevocable beneficiary and is entitled to the death benefit. In exchange, the lender advances a percentage of the death benefit to the policyholder during their living years. This strategy allows you to use your policy’s payout before you die. But, if you repay the loan during your lifetime, the lender removes themselves as the beneficiary.

How Can I Remove an Irrevocable Beneficiary?

Removing an irrevocable beneficiary requires their consent — but that’s the whole point! With this in mind, a policy owner should choose an irrevocable beneficiary carefully, if you select one at all. You don’t want to regret your decision down the road.

What is a revocable beneficiary?

A revocable beneficiary is a named beneficiary on your life insurance policy that you can change without their consent. If all your beneficiaries are revocable, you can freely modify or cancel your life insurance policy because no one else’s permission is required.

This flexibility is helpful in situations like the following: suppose you select your two adult children to each receive 50% of your death benefit. They’re both revocable beneficiaries.

As time passes, family dynamics can change. As the years go by, Child One visits you frequently and has taken responsibility for your care more so than Child Two.

In this example, you might want to change your death benefit to provide Child One with a larger payout. However, if both children were irrevocable beneficiaries, Child Two might object to this change and not provide their consent. Keeping your beneficiaries revocable keeps you in full control of who gets the payout.

Contingent beneficiary (secondary beneficiary)

Contingent or secondary beneficiaries only receive your death benefit if the primary beneficiary dies before or at the same time as you. Secondary and contingent beneficiaries are generally revocable beneficiaries.

Should a beneficiary be revocable?

When doing estate planning with your life insurance plan, it’s usually wise to make contingent beneficiaries revocable. This removes the burden of gathering numerous consents whenever you want to change your life insurance.

Even primary beneficiaries can be revocable. Doing so lets you remain in control of your life insurance policy.

As life changes, your priorities change as well. Accommodating these priorities is much more complex when you need one or multiple irrevocable beneficiaries to consent to policy changes.

What is the difference between revocable and irrevocable life insurance?

The main difference between revocable and irrevocable life insurance is how you make changes to the policy. A life insurance company requires your irrevocable beneficiary’s consent to make policy changes. In contrast, a revocable policy lets you change your life insurance around freely and without anyone else’s permission.

How often should I review my beneficiaries?

As a policy owner, it’s important to review your beneficiaries regularly. This ultimately depends on your own schedule, but many people do it once a year.

It is also beneficial to revisit your policy and its beneficiaries whenever you face a major life event. This could include a new home purchase, marriage, divorce, birth of a child, or even a family member’s death.

We understand that as your life changes, so do your insurance requirements. A PolicyAdvisor expert insurance advisor can help you set up a new policy or make changes to your existing one to meet your evolving needs. Schedule a call with a PolicyAdvisor insurance expert today!

A beneficiary is the person or organization that will receive your policy’s death benefit. A revocable beneficiary is someone you choose that can be changed at any time without their permission. An irrevocable beneficiary cannot be changed without the written permission of the irrevocable beneficiary.