- Simplified issue and guaranteed issue are types of no-medical life insurance

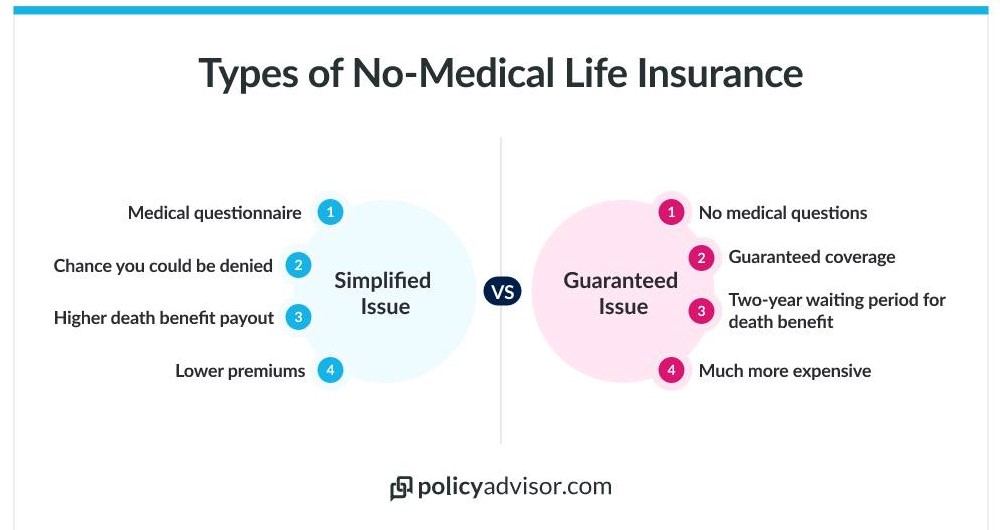

- Simplified insurance policies have better coverage options, but they ask health questions, so you can still be denied

- Guaranteed insurance policies do not ask health-related questions and cannot refuse you, but they're more expensive and coverage is limited

There are many different types of life insurance. Traditional life insurance policies usually have the best prices and coverage, but their applications are harder to approve because of their strict rules. Not everyone can qualify for them. But there’s another type called no-medical life insurance. This kind is easier to get because you don’t need to do a medical examination during the application process.

There are 2 main types of no medical life insurance: simplified issue and guaranteed issue. The right policy for you will depend on several factors. In this article, we’ll compare both to help you decide.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is simplified life insurance?

Simplified issue life insurance is a special kind of no-medical life insurance. It asks only a few health questions, and it doesn’t make you take a life insurance medical exam.

Like all life insurance policies, it’s an agreement between you and your life insurance provider. You pay money, called a life insurance premium, to the company. Then, if something happens to you and you pass away, the company gives money to your beneficiary. Your beneficiary can be family, a friend, a charity, or anyone you want. The money they receive, called a death benefit, is tax-free and can be used in any way your beneficiary would like.

Because the requirements for simplified issue policies aren’t as strict as standard policies, simplified is a good backup choice for:

Simplified life insurance comes in both term and whole life options. Term life insurance lasts a specific number of years (5, 10, 20 years, etc.). Whole life insurance lasts your entire life.

This type of policy may not have as many options as standard life insurance, but it still gives decent coverage for those who need it.

Simplified issue life insurance pros

✅ Easy approval. Because underwriting is not as strict, a lot of people can get this kind of coverage.

✅ Quick issue. The time between applying and getting a policy is much faster than standard life insurance.

✅ Level premiums. How much you pay every month or year won’t change as long as your policy is active.

✅ No medical exam. You only need to answer a few questions about your health to apply.

✅ Term or whole life coverage. This kind of insurance still lets you choose your policy length.

Simplified issue life insurance cons

❌ More expensive. There’s a higher financial risk involved for the insurance company when they give you a policy, so your premiums will be higher compared to standard life insurance, which has a full underwriting process.

❌ Limited amount of coverage. Many policies won’t provide more than $500K.

❌ Limited age range. Most providers won’t insure someone past age 75-80.

❌ Limited riders. Simplified plans only have a few add-on options, and it depends on your provider.

❌ You can be denied. Although requirements aren’t as strict, you can still be denied for simplified life insurance.

What is guaranteed life insurance?

Guaranteed issue life insurance is another kind of plan that doesn’t ask you to take a medical examination. Actually, this one doesn’t ask any questions about your health status at all. It’s called “guaranteed acceptance” life insurance.

The name is fitting because guaranteed life insurance guarantees you’ll get coverage — you can’t be turned down if you apply for it. Because of this, guaranteed insurance is a popular choice for people with severe health conditions who may not be able to get a traditional or simplified life insurance policy. But it’s often a last-resort choice because it can have a lot of downsides.

Guaranteed issue life insurance pros

✅ Simple application process. With guaranteed policies, you don’t have to answer any medical questions, so it’s easy to apply for.

✅ Guaranteed approval. Underwriting is the least strict — just about everyone can get this type of life insurance.

✅ Quick issue. The time between applying and getting a policy is much faster than standard life insurance.

✅ Level premiums. How much you pay every month or year won’t change as long as your policy is active.

✅ No medical exam. Guaranteed insurance doesn’t ask you to do a medical test.

✅ No health questionnaire. Guaranteed insurance also doesn’t require a medical questionnaire about your current health or health history.

✅ Guaranteed coverage. Once you sign up, you’ll definitely be approved.

Guaranteed issue life insurance cons

❌ Most expensive. Because these policies won’t say no to anyone, they cost more than both traditional life insurance and simplified issue insurance.

❌ Limited amount of coverage. Most policies won’t provide more than $50K.

❌ Limited age range. Most providers won’t insure someone past age 75-80.

❌ No riders. You cannot get add-on options at all with guaranteed life insurance.

❌ Limited types of coverage. You can only get permanent life insurance that lasts the rest of your life.

❌ Two-year waiting period. With this type of insurance, you have to wait 2 years before any payouts would be made.

What’s the difference between simplified issue vs guaranteed issue life insurance?

Although they are both types of non-medical life insurance, there are several differences between simplified issue and guaranteed issue life insurance policies:

- Underwriting

- Cost

- Type of coverage

- Coverage limits

- Riders

- Waiting period

Generally, simplified issue is a better choice than guaranteed issue, which we only suggest if someone does not qualify for any other type of insurance.

Should I get simplified or guaranteed life insurance?

The question of which type of insurance you should get depends on your unique needs, and which policy you would be most likely to get approved for.

Generally speaking…

Simplified issue life insurance is best if you:

- Are older in age

- Have a history of health concerns

- Have serious health issues

- Don’t want to do a medical exam

- Need life insurance quickly and don’t have time to wait for the traditional underwriting process

- Can’t get traditional life insurance products for some reason (health issues, dangerous occupation, or risky hobbies)

Guaranteed issue life insurance is best if you:

- Have severe health issues or a terminal illness

- Can’t get simplified life insurance

Normally, we suggest that people with health concerns try to get a simplified issue policy. It’s a better choice than guaranteed issue, which we only suggest if someone does not qualify for any other type of insurance.

A guaranteed policy may not be the best possible outcome, and may not provide as large a death benefit payout as you wanted. But at the very least it can give you peace of mind in knowing that your loved ones will be provided for to some degree if something unexpectedly happens to you. It’s often used as a form of burial insurance to cover an insured person’s funeral costs and any other end-of-life expenses.

Is deferred life insurance the same as simplified or guaranteed?

No, deferred life insurance is not the same thing as simplified or guaranteed issue. But, it might show up in your Google search if you’re looking at non-traditional types of insurance policies.

Deferred insurance plans are those where your loved ones aren’t paid the tax-free death benefit right away. Deferred insurance is not a specific type of insurance per se. Instead, it refers to insurance policies where the payment happens at a later time than it would for a standard insurance plan.

Guaranteed acceptance policies are a type of deferred insurance because you have to wait 2 years before the death benefit can be paid.

Are there other types of no medical life insurance?

Yes, there is one more kind of no medical life insurance besides simplified issue and guaranteed issue: accelerated issue.

Accelerated issue life insurance is a normal life insurance policy that you can get without doing a medical exam. The kicker is that you have to pass a strict questionnaire that asks you about your health history. Basically, the insurance company wants to find out if you have any health issues that could be risky. Having good medical records is very important if you want to apply for accelerated issue insurance.

With this kind of insurance, you can get up to $1 million in coverage. And you may even be able to get life insurance riders, depending on who your provider is. But the application process can be difficult, and there is a longer wait time before you hear back about whether you’re approved.

Get personal insurance help

If you’re still not sure if a simplified policy or a guaranteed policy would be best for you, contact us! Our friendly, licensed insurance agents can help you find the perfect plan based on your needs. We’d be happy to help provide more information so that you can make the best decision for your family.

Canadians who need no medical life insurance can typically choose simplified issue or guaranteed issue. Both types of policies don’t require a medical examination, but there are some key differences to know about. Simplified is usually more affordable and has more options. Guaranteed has fewer options, but cannot turn you down.