1-888-601-9980

1-888-601-9980

- Life insurance companies require a video or in personal call to confirm your identity

- You will be asked about your health and lifestyle to determine premiums and eligibility for coverage

- After your initial application, you may have to do a medical exam or tele-application to further determine your health history and risk

- What is on a life insurance application?

- Key sections of a life insurance application

- How to apply for life insurance?

- What to bring to the application call?

- Can you avoid a life insurance application interview?

- Do I have to tell the insurance company everything on a life insurance exam?

- Life insurance underwriting process

- Frequently asked questions

Insurers in Canada collect personal details, health related information, and financial information on a life insurance application to assess risk and determine an applicant’s eligibility. While the application itself is straightforward, the process and the steps involved can often seem overwhelming.

It is essential that you provide accurate and complete information while filling out a life insurance application. Failing to do so can lead to the insurer declining your application, or denying a claim that you make later.

If you’re feeling a little anxious about what to expect on your life insurance application, we’ve got you covered. We’ll go over how you can prepare for your life insurance application, what to bring, and how to make sure the process goes super smooth!

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is on a life insurance application?

A life insurance application typically includes basic identity questions, and some health and lifestyle information as well. This won’t involve a full interrogation about what you were doing on the second Thursday in March last spring. It’s just a basic, getting-to-know-you introduction to make sure that you meet the insurance company’s specific qualifications for coverage.

Health information on a life insurance application

One of the major factors that determines life insurance coverage and eligibility is your health status. Pre-existing conditions are taken into consideration and the underwriting process is usually stricter for those who have health issues.

Insurers assess the likelihood of a payout based on your health. To ensure that the policy works in your favour and will let them sustain their business, they may ask about some of the following factors:

- Your family’s health history: History of diseases that caused premature death. Information regarding frequency of cancers, strokes, diabetes, and other conditions

- Your health history: This includes the name dosages for any current medications and a list of diagnosed physical health conditions. They will also want to know about mental health diagnoses such as anxiety, depression, or bipolar disorder. If you have had previous conditions, they will ask about your doctor and any medical procedures or surgeries that you may have had in the past 10 years or more

Most life insurance applications require a follow up medical exam with your doctor to verify this information. This might also involve an additional tele-application as well. We’ll get more into that below.

Lifestyle details on a life insurance application

While it’s understandable to want to keep details about how you live your life private, insurance companies need to know if you’re engaging in activities that may potentially shorten your lifespan or lead to premature death. The riskier your lifestyle, the greater the risk the insurance companies will have to pay out sooner rather than later (when they’ve had a chance to collect premiums from you).

You may be asked:

- About your travel history in the last 2 years and any upcoming travel plans

- Your driving history (if you’ve been charged with reckless driving, suspended license etc).

- History of drug, smoking (including marijuana), or alcohol offenses (and general drug/alcohol history)

- If you’ve been found guilty of any crimes or if there are criminal charges pending

- If you engage in skydiving, racing, parachuting, scuba diving, mountain climbing, backcountry skiing, or any other high-impact/high risk activity

- If you’ve flown as a pilot or student pilot

About your occupation/income

At this stage of the application, the insurance company doesn’t need to see all your backtaxes from the last 10 years, but they do need to have some idea of how you handle your finances to make sure you can pay your premiums. They also need to know if the job you’re doing puts you at higher risk of being in harm’s way.

You may be asked:

- What your general occupation is

- If you’ve declared bankruptcy

- Information about collecting EI or CPP

Key sections of a life insurance application

The key sections in a life insurance application are typically to do with personal information, health and lifestyle details, policy details, and financial information. Here’s a detailed look at each:

- Personal information: Name, date of birth, address, phone number, and Social Insurance Number (SIN)

- Beneficiary details: Naming primary and contingent beneficiaries

- Policy type: Whether you’re applying for term or whole life insurance and the coverage details

- Health information: Detailed medical history with present and past health conditions, if any

- Lifestyle and occupation: Smoking, alcohol, and drug use, and income along with occupational risk assessment

- Financial information: Income details and net worth

How to apply for life insurance

Step 1 – Get a quote

Before you even get to the application process and paperwork, you want to make sure that you’re given a quote for the coverage that you’re looking for. The best place to begin is getting an instant, online quote at policyadvisor.com. You just have to enter a few basic details about yourself and our quoting tool will search across 20+ of Canada’s best insurance providers to find prices. You can then compare prices, adjust coverage, and select a quote that looks best for you.

Step 2 – Discuss the quote with an advisor

The next step is to speak to one of our licensed insurance advisors. Our team of experts has years of experience to guide you towards a policy that works for you and your family’s financial goals and needs. For some, this means choosing a policy that has lower premiums and for others, it might mean choosing a policy with a little higher premium with greater investment opportunities. Either way, we want to find a policy that works for you—we won’t upsell you on products you do not need!

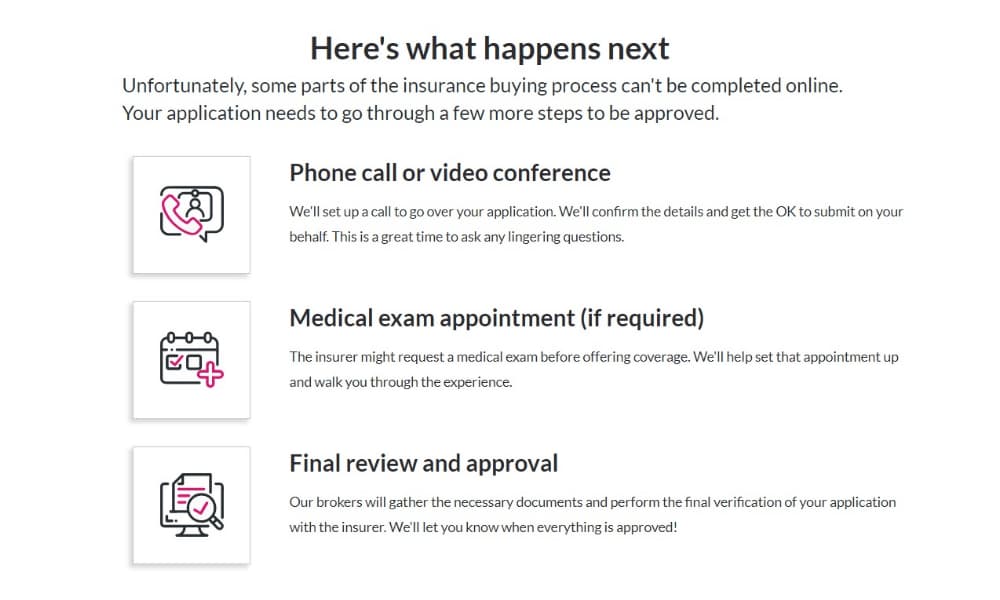

Step 3 – Schedule your application call

After this open conversation with our advisor team, you decide which company and policy you want to go ahead with. The advisor will then schedule you for an application call. Because we are an online brokerage, there’s no need to come down to an office or make travel arrangements—we’ll help you through the process in the comfort of your own home either via video chat or phone call. We do have to verify your identity though, so we will require a video call to check that you match your ID.

What to bring to the application call?

While your advisor should already have some basic information about your health and lifestyle from the initial quote, you may need to provide some more detailed information about your history. Some of the information you may know off the top of your head, but you’ll need to come prepared with some documents as well.

Here’s what you’ll need to bring to your appointment:

- Your driver’s license to verify your ID

- Your Social Insurance Number

- Citizenship documents

- Policy documents from other insurance policies (we want to make sure we’re not overinsuring you)

- Income details

In some cases, we may ask for photos of ID documents to verify your identity. If you are a non-resident of Canada, you can still apply for life insurance coverage but may have to provide additional documentation of your work permit, study permit, or refugee status. However, each application will be different and have different requirements, depending on which insurer you go with.

Can you avoid a life insurance application interview?

No, if you want life insurance you have to complete the application form and interview process. This is the case for both term life insurance and permanent life insurance. In order to place coverage, the insurance company needs to know information about you and your life to know if it’s in their best financial interest to insure you.

Do I have to tell the insurance company everything on a life insurance exam?

The short answer is yes—you have to answer all questions honestly. If it’s the case you leave something out or you lie on your application, a claim could be denied, which could be devastating to your family. For example, if you forgo information about a previous cancer diagnosis, and end up dying of cancer later in life, your insurance company may deny your beneficiaries from the death benefit, meaning you paid years of premium for nothing.

Life insurance underwriting process

Life insurance companies need to manage risk—they need to ensure that they can calculate the likelihood of your demise and when and if they might have to payout the death benefit. It does sound dark but it is necessary for insurers to calculate an accurate premium for you. They do this through an underwriting process where they factor in the following:

- Your age: The younger you are, the better. Young people are healthier and expected to live longer. Hence they get lower premiums compared to older individuals

- Health and lifestyle: If you smoke or have a pre-existing condition, your premiums will be higher since you’re at a risk of developing further issues that can be life threatening

- Gender: Women, on average, live six to eight years longer than men (source: World Health Organization). So, women generally see lower rates for life insurance

- Occupation: Jobs such as police officers, firefighters, construction workers, oil drillers, and loggers are among a long list of those who face more risks than others resulting in higher premiums. However, with increasing studies (National Library of Medicine) linking stress to higher mortality rates, having a high-stress office job may also affect your coverage

- Foreign travel: Frequent travelling or upcoming trips to dangerous countries can lead insurers to suspect a higher risk of death.

- Previous ratings: If you previously applied for life insurance and received a life insurance rating, your current application may consider this initial rating.

- Hobbies: Dangerous hobbies can mean higher insurance rates. Activities such as bungee jumping, paragliding, or skydiving may not be the best idea.

- Driving history: In 2018, Canada saw over 1,900 deaths as a result of motor vehicle accidents (source: government statistics). A poor driving record can, therefore, indicate a higher risk to the insurer

Life insurance medical exam

Once the insurance company knows a bit about your medical history, they’ll want to confirm everything with your doctor with a medical exam. During this exam, they may take your blood pressure, take blood samples, and record other information about your weight, height, medications.

A medical professional will administer these sample collections as well go through a detailed medical questionnaire that is administered by a life insurance provider. The doctor may call the provider to go through this tele-application and answer any further questions the insurance company has.

While a full medical exam is not mandatory by federal or provincial insurance laws, it may be an underwriting requirement, depending on the insurance company you’re going ahead with. If you’re feeling unsure about the hands-on portion of the application process, there are other policies—they involve fewer needles and ask a bit more questions than the standard medical life insurance, but you get less coverage at a higher cost. This type of insurance is called “no-medical” insurance or simplified life insurance.

Other than those who want to skip the needles, no-medical life insurance is also great for those who are declined because of pre-existing conditions or those with high-risk lifestyles who wouldn’t qualify for traditional life insurance.

If you’re short on time and want to skip the needles AND most of the medical questions, some carriers offer what is known as “guaranteed coverage.” However, it’s again usually more expensive and offers lower coverage amounts than traditional policies.

Read more about the difference between simplified and guaranteed life insurance.

Schedule a call

Whether you’re just toying around with the idea of a policy and are looking for quotes or are ready to jump right in, we’d love to chat with you. Our licensed insurance experts at PolicyAdvisor are available to assist you through the whole life insurance application process. We’ll answer questions, provide recommendations for coverage, and work to get you the best coverage at the best price from one of Canada’s top life insurance providers.

Frequently asked questions

What are the most important sections to focus on when filling out a life insurance application?

All the sections on a life insurance application should be carefully filled, especially when it comes to your personal and health related information. If you fail to provide accurate information, it might get flagged during the underwriting process. This could potentially lead to your application being declined. If you do get coverage and the insurer finds that your information was inaccurate during the application process, they will deny or delay payouts to your beneficiaries.

What should I do if I have a pre-existing medical condition when applying for life insurance?

If you have a pre-existing medical condition, you should be honest and inform your insurance advisor. There are life insurance plans that are specifically designed for those who have a pre-existing medical condition.

How can I ensure my beneficiaries are properly listed on the application?

To ensure your beneficiaries are properly listed on your life insurance application form you should provide accurate information such as their names, contact details, and your relationship with them. You should also assess your policy details periodically and update the beneficiary information if required.

What are the typical questions asked during the underwriting process?

During the underwriting process insurers will ask you about your health condition, lifestyle, occupation, previous insurance coverage details, financial information, and beneficiary information.

Life insurance companies collect information about your personal and health history to decide the financial risk to insure your life. After you get your quote and agree to apply, your agent will run through some basic questions to make sure you meet the insurance company’s requirements. Depending on your answers, the company will determine your premiums, eligibility, and coverage.