- Whole life insurance policies accumulate a cash value

- You can use this cash value to fund reduced paid-up insurance

- Reduced paid-up insurance means your guaranteed death benefit would only be your cash value, but you don’t have to pay any more premiums

- This option works for those who can no longer afford policy premiums, but still want to maintain some amount guaranteed death benefit

Reduced paid-up insurance lets you exchange your whole life policy for a reduced guaranteed death benefit that doesn’t require monthly payments. This type of policy is ideal if you’ve built a steady amount of cash value in your whole life policy and no longer want or can’t afford to pay your monthly premiums.

While this may seem like an easy way to utilize a whole life policy’s cash value and get away with not having to foot your insurance bill later in life, it may mean the death benefit your family gets is significantly lower than you originally planned. PolicyAdvisor is in the business of providing policies, but we also want to help you reach your financial goals. If you use your cash surrender value to purchase a reduced paid-up policy, it’s vital to understand the terms and conditions of the transactions and what your alternatives are.

This article explains the details of reduced paid-up policies and goes over situations where it may be beneficial for your financial situation.

What is reduced paid-up insurance?

A reduced paid-up insurance is a type of policy that results when you take the cash value of the policy as the death benefit, rather than the originally agreed-upon coverage amount from a whole life insurance policy. It’s “paid-up” meaning you won’t have to make further premium payments. However, the death benefit is usually reduced compared to the original whole life policy, depending on when you take this option. Some companies may require a certain amount of elapsed time before you can take this option, so it’s always best to check your policy wordings.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is a non-forfeiture clause?

Non-forfeiture clauses are an insurance option that is included in whole life policies that allow you to receive full or partial benefits or a partial refund of your premiums if you stop making payments, depending on which option you choose.

You could also receive other non-forfeiture options such as

- Receiving the cash surrender value as hard cash

- Purchasing extended-term life insurance, which converts the cash value of your whole life into a term life policy with the same death benefit – your whole life policy’s cash value generally determines the coverage period

- Using your accumulated cash value to pay your future premium

- Choose reduced-paid-up insurance, which uses your cash value as your new guaranteed death benefit.

Non-forfeiture clauses are available with universal life insurance, as well. However, with universal life policies, you choose a pre-selected investment portfolio based on your risk tolerance. As a result, the cash value of your universal life policy changes depending on the performance of the investment portfolio and can change the death benefit of a reduced paid-up policy or the term of an extended-term life policy.

Ultimately, non-forfeiture clauses are a great way to protect yourself in the event you’re unable to pay further premiums. It provides options on converting the cash value you’ve worked so hard to build.

How does reduced paid-up insurance work?

If you no longer want or can’t afford to pay premiums, you can use the non-forfeiture clause described above. A life insurance company can calculate a reduced coverage based on the cash value of your whole life policy and how much in premiums you’ve paid thus far.

You can only purchase a reduced paid-up policy with a permanent life insurance policy, like whole or universal life insurance. Read more about the differences between whole vs. universal life insurance.

Term life policies don’t provide a cash value that can convert into a reduced paid-up policy since the benefit is not guaranteed. You only get the death benefit from a term policy if you die within the allotted period or term.

Example of the reduced paid-up policy process

Suppose you purchased a whole life policy seven years ago with a death benefit of $200,000. It has built up significant cash value over this time—around $50,000.

You’re planning to retire in the next year. Your income will significantly drop, so you’ll have to reduce your monthly expenses as well. You speak with a life insurance advisor to see how you can reduce your monthly premiums.

In this discussion, your advisor might suggest using your whole life policy’s cash value to purchase a reduced paid-up policy. This reduces your guaranteed death benefit to $50,000 but also eliminates premium payments.

Such a solution is ideal for retirement because children are often grown up (meaning you no longer have financial dependents). Further, retirees commonly have little or no debts. If having a significant death benefit paid to your beneficiaries isn’t as important to you or you have estate funds saved up separately and you’d rather have the extra premium payments in your pocket, this might be a good option for you.

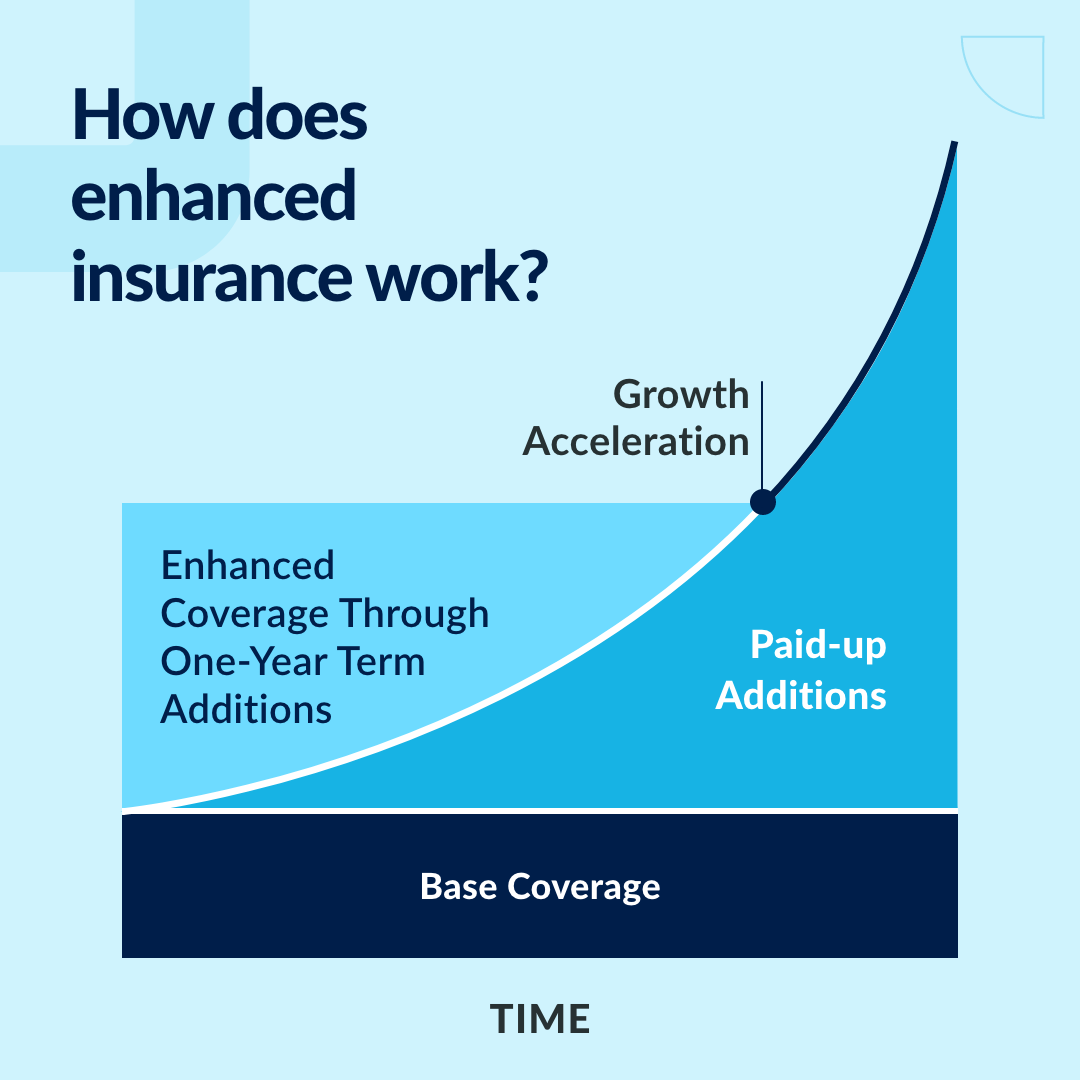

What’s the difference between reduced paid-up insurance and paid-up additions?

Reduced paid-up insurance is a type of life insurance policy you have when you forfeit your existing whole life policy. The death benefit of reduced paid-up insurance is only the cash value you accumulated while you when paying whole life insurance premiums.

Alternatively, paid-up additions let you swap your whole life policy’s dividends for additional life insurance coverage. Unlike reduced paid-up insurance, you still pay the monthly premium to your original whole life policy, as your whole life policy is still in force, just with an increased death benefit amount.

Paid-up additions are usually bought as a policy rider to your initial whole life insurance purchase. A rider is an optional add-on that supplements your whole life policy. In contrast, reduced paid-up insurance is a non-forfeiture clause option.

Ultimately, paid-up additions are for someone who wants a larger death benefit without paying additional premiums. Reduced paid-up insurance is often for someone who wants to retain some amount of death benefit without paying any premiums at all.

What’s the difference between reduced paid-up insurance and extended-term insurance?

Extended-term policies provide a term life insurance policy that no longer requires premium payments. The cash value that has been accumulated from a whole life insurance policy is used to purchase term life insurance with a death benefit as close to your original whole life death benefit as possible. Because it’s a term life policy, the death benefit is only payable if you pass away during a particular period. In contrast, a reduced paid-up policy guarantees a death benefit.

For example, say you had a whole life policy with a death benefit of $100,000 and an accumulated cash value of $10,000. With extended-term policies, the insurance provider would calculate how many years it would take for premium payments of $10,000 (your cash value) to equal $100,000 (your death benefit) in coverage. Say this takes 20 years. Therefore, you would exercise the non-forfeiture clause to purchase a term 20 policy with a death benefit of $100,000 and pay no premiums at all—it’s already paid for by your cash value.

The two policies are similar in that the cash value of your original whole life policy is converted into another life insurance product without the need to pay premiums. They’re also both options in a non-forfeiture clause.

You might choose an extended-term policy because you want a larger death benefit but don’t have enough cash value in your whole life policy to afford such a payout with a reduced paid-up policy. Extended-term insurance tries to match your original death benefit, whereas the reduced paid-up death benefit is only your cash value.

An extended-term policy is also beneficial if you only need a death benefit for your beneficiaries if you die within a specific timeframe — for example, while your children are still in school or until your mortgage is paid off.

Should you purchase paid-up insurance?

Reduced paid-up insurance is a good option if you don’t want to continue premium payments but still want a death benefit for your beneficiaries. Just remember that the death benefit is usually reduced when compared to your whole life policy’s original payout amount.

This type of insurance is ideal if you no longer need the total amount of your whole life policy’s death benefit because you have fewer debts and/or financial dependents now. You might also consider it if you can no longer afford your whole life insurance premiums.

Whether you should purchase a reduced paid-up policy depends on your life circumstances, similar to any life insurance policy. Speak to one of PolicyAdvisor’s licensed insurance advisors today to determine whether a reduced paid-up insurance policy is right for you.

The information above is intended for informational purposes only and is based on PolicyAdvisor’s own views, which are subject to change without notice. This content is not intended and should not be construed to constitute financial or legal advice. PolicyAdvisor accepts no responsibility for the outcome of people choosing to act on the information contained on this website. PolicyAdvisor makes every effort to include updated, accurate information. The above content may not include all terms, conditions, limitations, exclusions, termination, and other provisions of the policies described, some of which may be material to the policy selection. Please refer to the actual policy documents for complete details. In case of any discrepancy, the language in the actual policy documents will prevail. All rights reserved.

If something in this article needs to be corrected, updated, or removed, let us know. Email editorial@policyadvisor.com.

If you have a whole life insurance policy and no longer want to pay premiums, you may use your cash value to fund reduced paid-up insurance. This means that you can choose to stop paying premiums and your guaranteed death benefit would be the cash value, rather than the original agreed-upon coverage amount. Reduced paid-up insurance is different from paid-up additions, which is additional insurance that can be purchased using policy dividends.