1-888-601-9980

1-888-601-9980

- Permanent life insurance policies such as whole and universal life insurance accumulate a cash value

- This cash value builds as the insurer invests a portion of your premiums

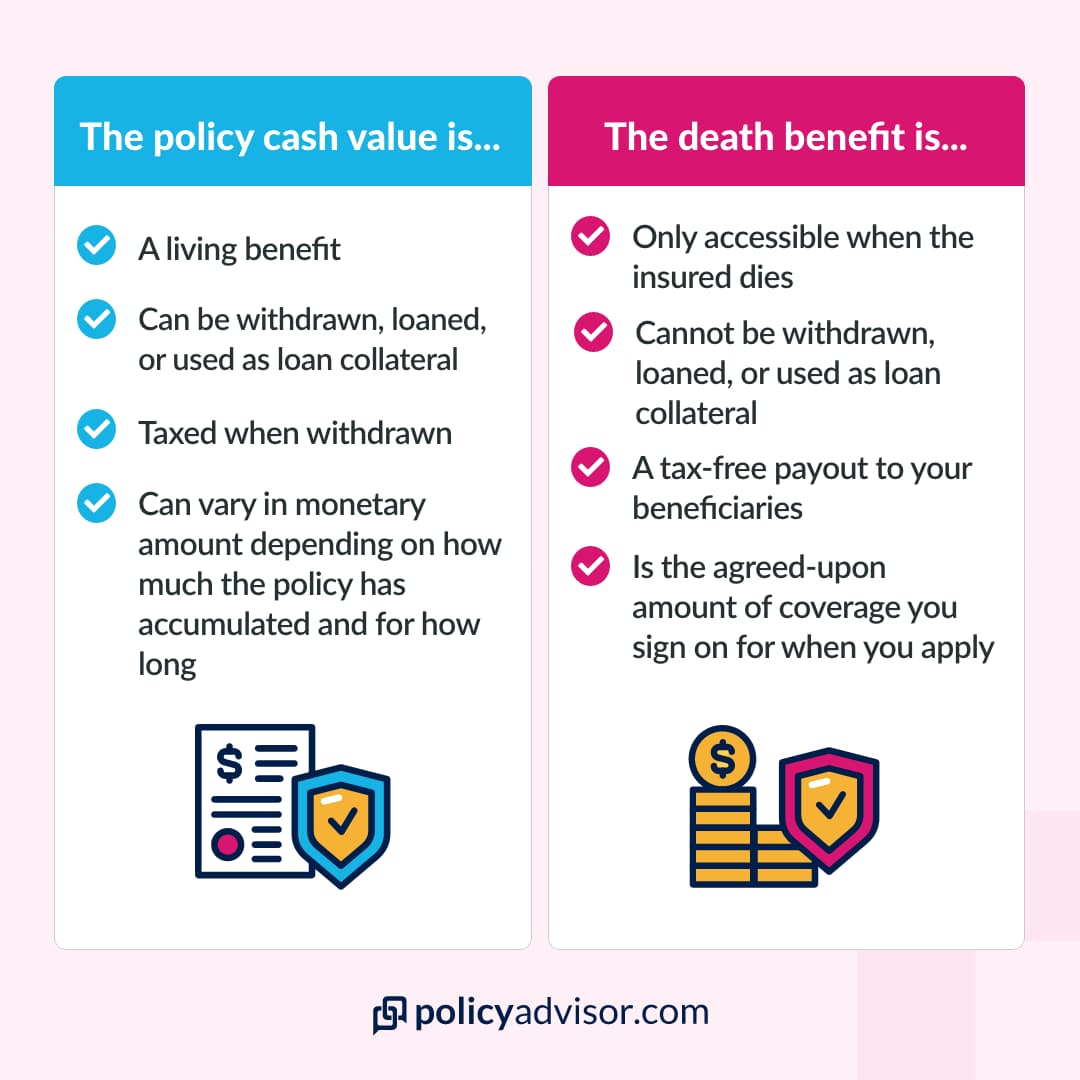

- The cash value is not the same as the death benefit and your beneficiary will not get both values, only the death benefit

- With some policies, you can use the cash value to loan against, withdraw, or reinvest back into the policy

- What is cash value life insurance?

- How does cash value work in a whole life insurance policy?

- What is the difference between a policy’s cash value and its death benefit?

- How long does it take to build cash value on life insurance?

- How can you access the cash value?

- What are the benefits of cash value life insurance in Canada?

- What are the drawbacks and limitations of cash value life insurance?

- Is a life insurance policy with cash value is right for you?

- Frequently asked questions

If you are in the market for a permanent life insurance policy, you may have noticed that many policies highlight the added living benefit of something called cash value. The following article will illuminate the concept of cash value and demonstrate how it can be used as a strategic part of long-term financial planning. Cash value provides an opportunity for you to benefit you now and your family’s future later.

What is cash value life insurance?

Cash value is included with certain types of permanent life insurance, like whole life insurance and universal life insurance. Your insurance provider places a portion of your premiums into a savings account or investment portfolio. Essentially, cash value is a sum of money that builds up over the course of your life insurance policy—it’s what your policy is worth.

Every time you pay your policy premiums, a portion of the money goes towards paying for your death benefit, a portion goes to fees, and another portion is earmarked for investment. This money—the cash value—typically increases over time due to interest and investment earnings. Policyholders can choose to withdraw their cash surrender value or can take out loans using their policy’s cash value as collateral.

Additionally, life insurance cash values grow on a tax-deferred basis, meaning they are not subject to tax until funds are withdrawn. We’ll talk about that more in later sections.

Some policies, including participating whole life insurance and universal life insurance, generate additional funds from their cash value dividends that the policyholder can utilize to pay their insurance premiums, invest back into the policy as additional death benefit coverage, or for further investment.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

How does cash value work in a whole life insurance policy?

Cash value is a unique feature of whole life insurance that functions as a savings component within the policy. When you pay your premiums, a portion goes toward building the cash value, which grows over time on a tax-deferred basis.

This means you won’t owe taxes on the growth unless you withdraw funds. Whole life policies typically guarantee a minimum rate of return on the cash value, providing consistent and stable growth regardless of market fluctuations.

One of the significant advantages of cash value is its accessibility. Policyholders can tap into it through loans or withdrawals. Loans are often tax-free but must be repaid with interest to avoid reducing the death benefit. Withdrawals may be taxable if they exceed the total premiums paid into the policy.

Over time, the cash value can serve various purposes, such as funding emergencies, supplementing retirement income, or covering premium payments. This combination of guaranteed growth and financial flexibility makes cash value an attractive feature for long-term planning.

What is the difference between a policy’s cash value and its death benefit?

There are a couple of key differences between a life insurance policy’s cash value and the death benefit. The death benefit is the money paid to a policy’s beneficiary when the named insured dies. Life insurance companies will issue a death benefit as long as policy terms are met and the insured person dies during their coverage period.

Unlike the death benefit, cash value can be accessed while the policyholder is still living. For this reason, it falls into the category of a “living benefit.” This means that the policy’s cash value is intended for use by the policyholder, whether the money is withdrawn during their lifetime or used for loans.

Another difference between the two is the gains made on the cash value of a policy can be treated as taxable income when they have been withdrawn, whereas beneficiaries do not have to pay taxes on a death benefit they receive.

How long does it take to build cash value on life insurance?

In general, it can take at least a decade to build up substantial cash value for a whole or universal life insurance policy. This is because it takes time for the cash value (what you pay through premiums) to accumulate and begin earning investment income and/or interest. After 10-15 years, the cash value of a policy will begin to grow at greater rates.

That being said, if accelerating the growth of your policy’s cash value is a priority, you have a couple of options. For instance, you can choose a limited pay whole life insurance policy. Some options include condensing your life’s worth of premiums into an 8, 10, 15, or 20-year-pay plan.

Because your premiums are paid up earlier, that money is used to invest earlier in the policy’s lifespan, meaning there is more time for the investment to grow.

How can you access the cash value?

There are a few ways to access your life insurance policy’s cash value: you can withdraw money, use it for loans, use it to pay your premiums, or surrender your policy for cash. In each scenario, there are some things to take note of.

Withdrawals

While withdrawing money from your policy’s cash value is an option, there are caveats. Depending on the size of the withdrawal (relative to the cash value) and the terms of your policy, you may be charged income tax on the money you take out.

Life insurance companies may also reduce your policy’s death benefit when you withdraw from the cash value, and there is no way to pay it back.

Policy loans

It is possible to access your policy cash value by taking out a loan from your life insurance provider. This type of loan typically has lower interest rates than a more traditional bank loan.

If you do take out a loan and do not pay it back before you die, life insurance companies will deduct the outstanding debt (including interest) from the death benefit.

You may also use your life insurance policy’s cash value as loan collateral for a bank loan, but the bank will have it’s own rules and stipulations regarding how much of the cash value they will allow as collateral (usually 50-90% of the cash value).

Surrendering your policy

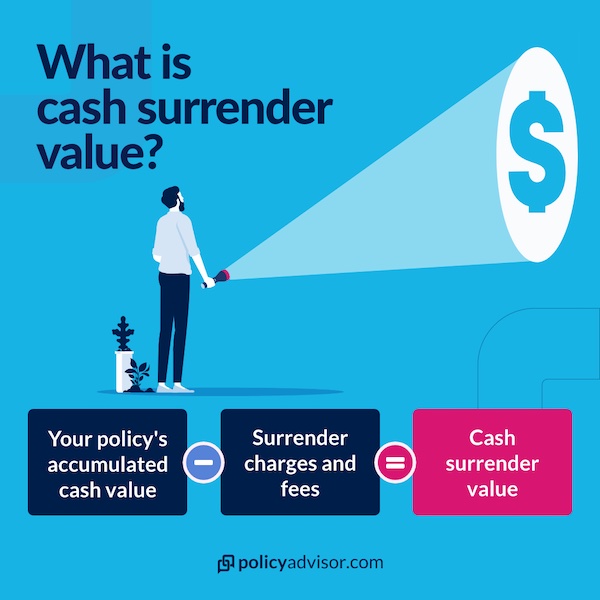

If you surrender your policy for cash value, you are essentially ending your life insurance contract (thus giving up the death benefit) to receive the cash surrender value. The cash surrender value is the policy’s cash value minus any processing and surrender fees.

Do you have to pay back cash value life insurance?

In general, you are not obligated to pay back policy loans or withdrawals of cash value from your life insurance policy. Any amount you withdraw or borrow directly from the policy will simply be deducted from your final death benefit (plus interest).

However, if you use the cash value as collateral on a bank loan, you will be required to pay back that bank loan, in which case the bank will either require you to forfeit the policy for it’s cash value or they will settle the loan using your policy’s death benefit, as in the loan process they have named themselves as the beneficiary.

Can you cash out life insurance before death?

Yes, you can cash out whole life insurance before death through the policy’s cash value. Options include taking collateral loans, policy withdrawals, or surrendering the policy for its accumulated value. However, these actions may reduce the death benefit or have tax implications.

What happens to the life insurance cash value at death?

When a policyholder dies, their beneficiaries will receive the policy’s death benefit, but not the cash value. In general, whatever money remains in the policy’s cash value will go to the life insurance company. That’s why it is important to use your policy’s cash value strategically while you are living.

In some cases, life insurance companies will allow policyholders to transfer their policy’s cash value to the death benefit, increasing what they will leave behind for loved ones, but this must be arranged prior to the policyholder’s death.

How long does it take for a whole life policy to build cash value?

The cash value of whole life insurance starts building from year one of the policy, but it typically takes a whole life insurance policy 10 years or more to build significant cash value. In the early years, most premiums go towards administrative costs and the death benefit, with a smaller portion going toward the cash value.

Over time, the cash value grows steadily. In some cases, dividends provide more accessible funds later in the policy.

What are the benefits of cash value life insurance in Canada?

Cash value life insurance offers a unique blend of lifelong coverage and financial flexibility, along with other benefits like access to cash value, guaranteed savings growth, and estate planning advantages, making it a valuable financial planning tool for Canadians.

- Lifelong coverage: Unlike term life insurance, cash value life insurance provides protection for your entire life as long as premiums are paid, ensuring your loved ones receive a guaranteed death benefit

- Tax-deferred growth: The cash value component grows on a tax-deferred basis, allowing your savings to accumulate more efficiently over time. This is especially beneficial for Canadians looking to build long-term wealth

- Access to cash value: Policyholders can access the cash value through loans or withdrawals. These funds can be used for various purposes, such as funding education, supplementing retirement income, or covering emergencies

- Guaranteed savings growth: Whole life policies often guarantee a minimum growth rate for the cash value, providing stability and predictable returns regardless of market conditions

- Financial flexibility: The ability to borrow against your policy or use the cash value to pay premiums provides financial flexibility during times of need or as part of retirement planning

- Estate planning advantages: The death benefit is generally paid out tax-free to beneficiaries, making it an effective tool for estate planning and ensuring a financial legacy

What are the drawbacks and limitations of cash value life insurance?

While cash value life insurance offers lifelong coverage and a savings component, it has some drawbacks and limitations such as high premium costs, slow initial growth, complexity, opportunity costs, and surrender charges that buyers should consider:

- High premium costs: Cash value life insurance is significantly more expensive than term insurance, making it less accessible for individuals on a tight budget

- Slow Initial growth: In the early years, most of the premium goes toward administrative costs and the death benefit, resulting in minimal cash value accumulation

- Complexity: The combination of life insurance and investment can be confusing. Understanding how cash value grows, loan terms, and surrender charges requires careful attention

- Opportunity cost: Premiums paid into the policy may yield lower returns compared to investing the same amount in higher-performing investment vehicles like stocks or mutual funds

- Surrender charges: Cancelling the policy early can result in significant surrender charges, reducing the available cash value

When does it make sense to purchase a cash value policy?

In deciding whether a cash value life insurance policy is right for you, it is important to think about your priorities. If you’re looking for a simple, inexpensive way to protect your loved ones financially should you die unexpectedly, a permanent life insurance policy with cash value may not be your best option.

If you are seeking to use life insurance to achieve long-term financial goals, a policy with cash value is highly advantageous. For instance, many people purchase whole life insurance with a view to supplement their retirement incomes using the dividends generated by the policy’s cash value.

Cash value life insurance also provides a tax-protected investment option. This means that your investment will continue to grow untaxed until it is withdrawn. Even then, you are taxed only on gains. Similarly, some loans taken out against a life insurance policy’s cash value are not subject to tax while the policy remains active.

All that being said, permanent life insurance policies with cash value are substantially more expensive than term life insurance policies. For that reason, they are often chosen by high earners to both pass along wealth to beneficiaries through the death benefit and generate investment income.

Is a life insurance policy with cash value is right for you?

Deciding which life insurance policy is the best depends on you and your family’s financial goals. There is no one-size-fits-all plan, unfortunately—that would make our job way too easy. Permanent life insurance policies with cash value options do come at a higher premium cost compared to term life insurance plans, but they can be extremely beneficial for those looking for a guaranteed death benefit with the added bonus of investment opportunities.

Let’s have a chat about your financial goals. Book a call with one of our licensed life insurance advisors at PolicyAdvisor today! We work with over 30 of Canada’s best life insurance companies and can shop around to make sure you get the policy that’s right for you!

Frequently asked questions

How is the cash value of life insurance taxed in Canada?

The cash value of life insurance in Canada grows on a tax-deferred basis, meaning you won’t pay taxes on the growth as long as it remains within the policy.

However, withdrawals or policy loans may trigger taxes if the amount withdrawn exceeds the adjusted cost basis (ACB)—the total premiums paid into the policy. Upon surrendering the policy, any gains above the ACB are taxable as income. Proper planning can help maximize the tax advantages of cash value life insurance.

Can you use the cash value as collateral for a loan in Canada?

Yes, the cash value of a life insurance policy can be used as collateral for a loan in Canada. This is often referred to as a collateral assignment. Many lenders accept the cash value as security, allowing you to access funds without surrendering the policy.

The loan amount typically depends on the cash value available. Using cash value as collateral lets you retain the policy benefits, but it’s important to ensure loan repayment to avoid affecting the policy’s death benefit.

What happens to unused cash value in participating whole life insurance?

In participating whole life insurance, unused cash value remains within the policy and continues to grow on a tax-deferred basis. At the policyholder’s death, the cash value does not typically get paid out in addition to the death benefit.

Instead, the insurer retains it, and only the death benefit is provided to beneficiaries. However, dividends earned on the policy can increase the death benefit or cash value, depending on the dividend option chosen by the policyholder during their lifetime.