1-888-601-9980

1-888-601-9980

- Visitors to Canada insurance is essential for visitors on a visit visa, parents visiting on Super Visa, international students, work permit holders, new immigrants on PR, and returning Canadians

- Canadian visitors insurance plans typically cover a range of medical expenses, including hospital stays, emergency medical transportation, and outpatient care

- The average cost of visitor health insurance for travellers to Canada typically ranges from $50 to $400 per month, depending on factors such as age, duration of stay, and the level of coverage chosen

- The Canadian government recommends at least a $100,000 coverage amount for visitors to Canada insurance plans

- What are the types of visitor insurance in Canada

- What does visitor insurance cover?

- What are some common exclusions to visitor insurance in Canada?

- Who needs visitor health insurance in Canada?

- How much does visitor health insurance cost in Canada?

- Which companies offer visitors to Canada insurance?

- How can I pay for Canadian visitors' insurance?

- Is visitors' insurance in Canada refundable?

- Can I get insurance for visitors to Canada with a pre-existing condition?

- Can I pause a visitor's insurance plan to travel back home?

- Frequently asked questions

Visitors to Canada insurance is a travel medical insurance designed specifically for non-residents visiting Canada, to provide coverage in case of any medical emergencies. Visitors to Canada insurance is essential for visitors on a visit visa, parents visiting on Super Visa, international students, work permit holders, new immigrants on PR, and returning Canadians who are not yet eligible for Canada’s provincial healthcare.

Since the Canadian healthcare system does not cover visitors, in case of an emergency the medical cost can be substantial. A visit to the doctor or a walk-in clinic could be anywhere from $100 to $600, while an emergency room or hospitalization could be as high as $6,000 per day!

What are the types of visitor insurance in Canada?

Visitor insurance in Canada plans typically have three major coverages: medical insurance for visitors to Canada, trip cancellation and interruption insurance, and Super Visa insurance.

Medical insurance for visitors to Canada covers eligible emergency health emergencies that a non-resident might develop during their trip to Canada.

Trip cancellation and interruption insurance offers financial protection and refunds in case of trip cancellation or modification due to any unforeseen circumstances.

Super Visa insurance is a specialized product that covers parents and grandparents of Canadian citizens and permanent residents who are visiting Canada for a minimum of 12 months and a coverage of at least $100,000.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Can I get health insurance as a visitor in Canada?

Any non-resident who is visiting Canada can get a health insurance for visitors to Canada insurance plan. International students, returning Canadians, and foreign workers who are yet to receive provincial healthcare benefits are also eligible for medical insurance for visitors in Canada.

Can a visitor in Canada see a doctor?

Yes, visitors in Canada can see a doctor, either in a hospital or a clinic. However, doctor visits are expensive, sometimes going upwards of $300. Medical insurance for visitors in Canada covers the cost of a visit to a doctor.

How can I see a doctor in Canada without insurance?

If you do not have insurance and want to see a doctor in Canada, you can simply visit the emergency room of your nearest hospital or a walk-in clinic. Hospitals in Canada are legally required to provide medical care regardless of a patient’s insurance or immigration status.

You can also choose to visit a pharmacy to purchase over-the-counter medicines and if you can afford it, you can go to a private practitioner who may accept cash. However, keep in mind that costs can greatly vary and healthcare in Canada is generally expensive, especially without visitor insurance.

What does visitors insurance in Canada cover?

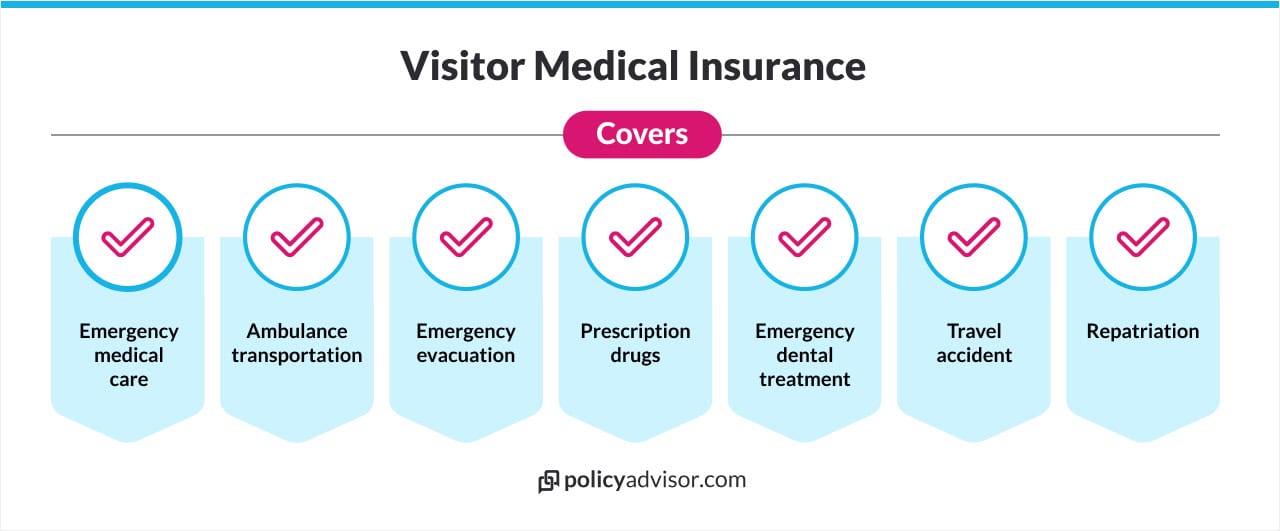

Medical insurance for visitors to Canada typically covers emergency medical procedures and services including hospital, emergency room, and walk-in clinic visits, doctor’s consultation, prescription drugs, diagnostic tests and scans, repatriation, and more.

The following is a list of commonly covered situations for a visitor to Canada insurance plan:

- Physician consultations: Doctor’s or physician’s fee and in some cases, follow-up visits with the doctor

- Prescription drug coverage: Cost of medicines prescribed for an emergency that occurs after the policy has come into effect

- Pathological tests or diagnostic procedures: Coverage for various diagnostic procedures including blood work, X-rays, CT scans, MRI, and more. The diagnostic tests and scans should be related to the medical emergency that occurs after the policy’s start date

- Paramedical services: Services by licensed professionals such as physiotherapists, chiropractors, podiatrists, or massage therapists. These services are covered if they are necessary due to a medical emergency

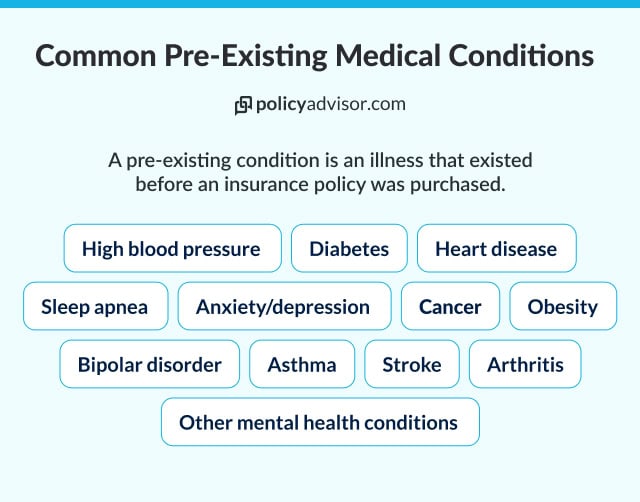

- Pre-existing condition coverage: Some insurance plans offer coverage for pre-existing conditions, which can be crucial for visitors with ongoing health issues

- Emergency dental care: Some insurance plans provide coverage for emergency dental treatment or surgery that may have resulted from an accident or sudden injury

- Accidental death and dismemberment (AD&D): One-time lump sum amount in case of severe accidents that may lead to the death or loss of limbs of the insured

- Ambulance transportation: Visitors’ health insurance covers the costs of ambulance services—whether ground or air—needed to transport the visitor to the nearest hospital or medical facility during a medical emergency

- Repatriation: Insurance can cover the costs of emergency medical evacuation back to your home country, which can be a significant cost without coverage

- Hotels, meals, taxis: If a medical emergency requires a visitor to extend their stay in Canada for treatment or recovery, the insurance can cover additional expenses for hotels, meals, and local transportation such as taxis

- Childcare: If a visitor is hospitalized and unable to care for their dependent child, the visitor to Canada insurance may cover temporary childcare expenses. This ensures the child is safe and looked after while the insured individual receives necessary medical treatment, providing peace of mind during a stressful time

- Trip break/Side trip: Some emergency medical insurance plans for visitors offer flexibility with a trip break or side trip coverage, which allows visitors to return to their home country for a short period or travel to another country without losing their insurance coverage

What are some common exclusions to visitor insurance in Canada?

Most medical insurance plans for visitors to Canada do not cover pre-existing conditions, pregnancy, mental health conditions, high-risk adventure activities, and anything that falls outside the Usual, Customary, and Reasonable (UC&R).

Common exclusions to a visitor insurance plan

| Exclusion | Details |

| Pre-existing conditions | Any unstable pre-existing condition |

| Non-emergency procedures | Planned surgeries, elective treatments, routine check-ups, alternative medication, and preventive care |

| Diagnostic tests | Diagnostic tests such as magnetic resonance imaging (MRI), computerized axial tomography (CAT) scans, ultrasounds, biopsies, etc. are only covered in extreme emergencies and must be pre-authorized |

| Pregnancy and maternity care | Pregnancy and maternity care are not included in visitor to Canada insurance plans. Some insurers may offer pregnancy care only under an extreme emergency |

| Mental health conditions | Mental health services, including counselling, therapy, and psychiatric care, and any ongoing treatment for mental health conditions are often excluded from visitor insurance policies |

| Drugs and alcohol related illness or injury | Incidents or illnesses resulting from chronic usage of drugs, alcohol, or other narcotics are generally excluded from visitor insurance coverage |

| High-risk activities | High-risk activities such as extreme sports (skydiving, scuba diving, bungee jumping), motor racing, and mountaineering are often excluded from visitors’ insurance coverage. Tugo is the only insurance provider that offers a Sports and Activities Coverage add-on that can provide substantial coverage if you participate in some risky activities |

| Self-inflicted injuries | Self-inflicted injuries, including those resulting from attempted suicide or any form of self-harm, are typically excluded from visitor insurance policies |

| Anything outside the usual, customary, and reasonable | Insurance companies maintain a database of UC&R for various provinces and review the claims based on it. If the claim is excessively higher than the standard cost of the treatment, they will not provide coverage for it |

| War and terrorism | Injuries or illnesses resulting from acts of war or terrorism are not covered |

| Aviation-related injuries | Any death or injury sustained while piloting an aircraft, learning to pilot an aircraft, or acting as a member of an aircraft crew is excluded |

| Injury or illness due to non-compliance with prescribed treatment | Not following recommended or prescribed therapy or treatment can void coverage |

| Side-trip against travel advisories | If an insured non-resident takes a side trip to a country that the Canadian government has issued a travel advisory for, any illness or injury as a result of that trip will not be covered under a visitor to Canada insurance plan |

Note: Insurance providers have their lists of exclusions to a visitor in Canada insurance plan. It is important to read your policy document carefully to ensure compliance.

Who needs visitor health insurance in Canada?

Any non-resident in Canada, including those visiting relatives, tourists, foreign workers, international students, and returning Canadians need visitor health insurance. Such a policy will ensure they are protected against significant costs associated with any medical emergency during their trip.

Visitor insurance for international students in Canada

Insurance providers such as Secure Travel (RIMI), Tugo, and Travelance offer customized visitor insurance plans for international students on student visas in Canada. To get a student’s visitor insurance policy applicants must be:

- Residing in Canada on a temporary basis

- Ineligible for benefits under a government health plan

- A student with proof of full-time admission in a recognized Canadian institution of learning; or

- A student completing postdoctoral research in a recognized Canadian institution of learning; or

- The spouse or dependent child of the insured student and residing with them on a full-time basis; or

- The parent, legal guardian, teacher or chaperone of the insured student

Visitor insurance to Canada plans for students cover everything that a medical insurance visitor plan covers. Some insurers such as Secure Travel (RIMI) also include coverage for emergency psychiatric care, trauma counselling, sexual health consultation, and tutorial services in case of illness as part of their student visitor to Canada plans.

Visitor health insurance for foreign workers in Canada

Foreign workers on a work permit who are not covered under any government health plan or an employer-sponsored plan can benefit greatly from a health insurance for visitors to Canada policy.

Visitor insurance in Canada is especially important for:

- Workers who have just arrived in Canada and are yet to receive provincial healthcare benefits

- Those whose work permits may have expired but they haven’t left Canada yet

- Workers who are in the process of getting their work permit renewed

Visitor insurance for returning Canadians

Canadians who have been living out of Canada for more than six months usually end up losing their provincial healthcare benefits. When they return to Canada, their government health coverage takes up to 2-3 months to be reinstated in provinces like Ontario, British Columbia, and Quebec.

During the waiting period, returning Canadians can benefit greatly from a visitors to Canada insurance plan to cover unexpected medical costs.

Canadians who move from one province to another also lose access to their government health benefits temporarily. Visitor to Canada plans can help them manage emergency medical conditions.

Insurance for parents and grandparents of Canadian citizens

Super visa insurance is a special type of visitor health insurance that’s only available to the parents and grandparents of Canadian citizens or residents who are staying in the country for a long period of time. This health insurance covers the any medical emergencies that happen during the visitors stay in Canada

The minimum requirements a super visa insurance policy has to meet are:

- Must be valid for at least one year from the date the visa-holder arrives in Canada

- Must have at least $100,000 in coverage

- Must cover emergency medical care, possible hospitalization, and repatriation

- Must be active and available for review by an immigration official each time the visa-holder enters Canada

- Must have been bought from a Canadian insurance company

Can I buy visitor insurance after arrival Canada?

Yes, you can buy visitor insurance after you arrive in Canada but more insurers will impose a waiting period, typically between 48 hours to 8 days. This waiting period is applicable for illnesses. Coverage for injuries typically begins as soon as the visitor insurance policy is purchased.

Insurance companies also have a purchase window where you have to buy visitor insurance within 30-45 days of your arrival in Canada.

How much does visitor health insurance cost in Canada?

The average cost of visitor health insurance for travellers to Canada typically ranges from $50 to $400 per month, depending on factors such as age, duration of stay, and the level of coverage chosen. For instance, younger travellers (under 40 years) may pay between $50 and $100 monthly, while those aged 70 years and older may see costs rise between $200 and $400 per month.

Factors that can influence the cost of medical insurance for visitors to Canada include:

- Age: Younger travellers (under 40) can expect to pay lower premiums as they are considered lower risk for health issues

- Pre-existing conditions: If you have pre-existing medical conditions, you will have to get a plan with coverage for pre-existing conditions. These plans are more expensive than plans without pre-existing conditions. Some insurers may charge a higher premium for pre-existing conditions plans, while others might exclude these conditions altogether

- Length of stay: The longer you stay in Canada, the higher the cost of insurance

- Coverage amount: Policies with lower coverage (e.g., $50,000) are more affordable but may not cover all potential medical expenses. Higher coverage limits (e.g., $100,000 or more) offer more extensive protection but come with a higher premium

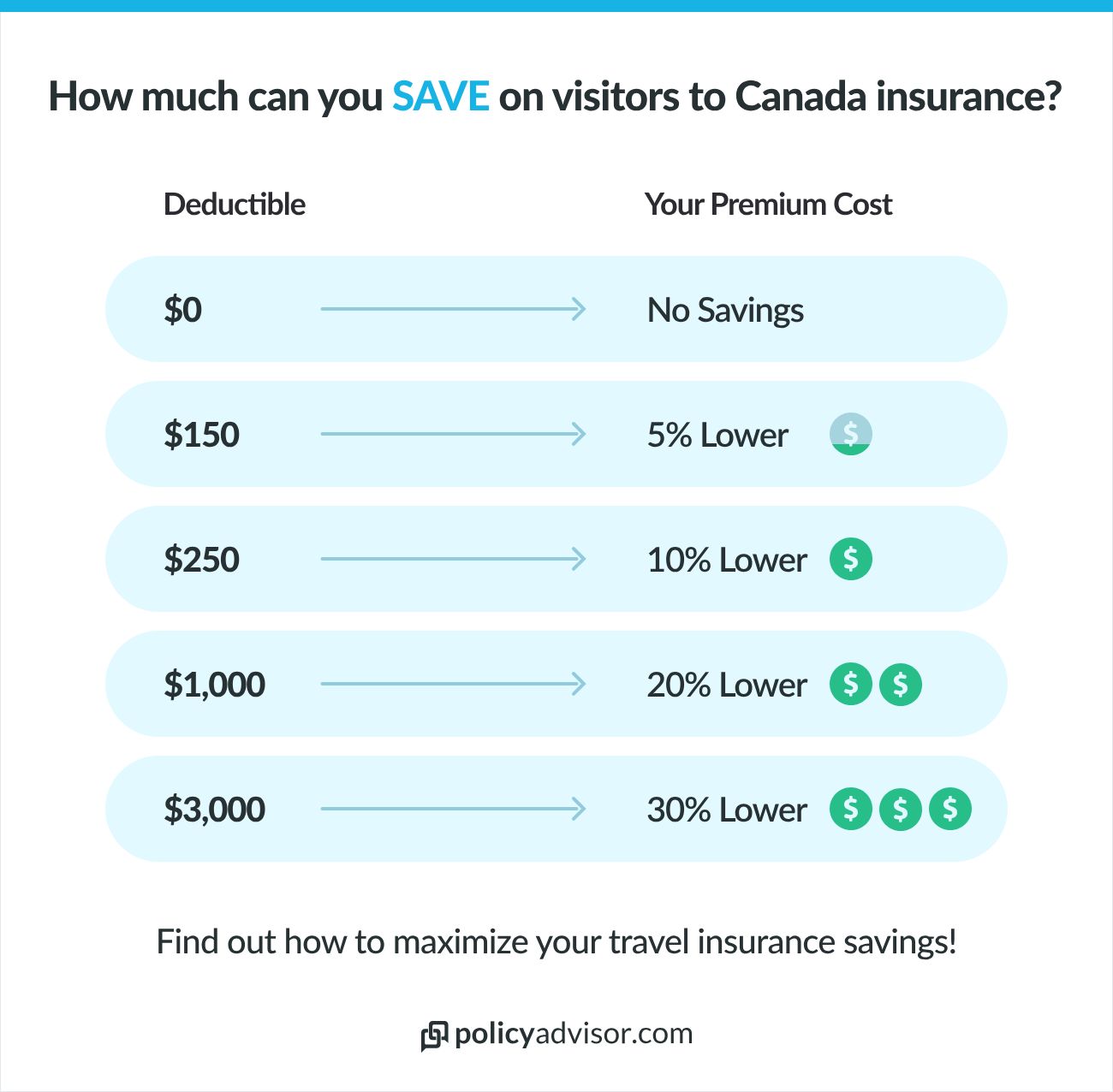

- Deductibles: High deductibles will have lower premiums and lower deductibles will lead to high premiums

How much coverage should I get for visitors to Canada insurance?

The Canadian government recommends at least a $100,000 coverage amount for visitors to Canada insurance plans. Healthcare in Canada is expensive—a visit to the doctor or a walk-in clinic could be anywhere from $100 to $600, while an emergency room or hospitalization could be as high as $6,000.

Getting adequate medical insurance for visitors to Canada coverage will help non-residents avoid paying out-of-pocket costs for emergency medical treatment.

What is a deductible for visitors’ insurance?

A deductible is the amount you need to pay out-of-pocket for your medical expenses before your insurance starts covering the costs. For example, if your deductible is $500, you’ll need to pay the first $500 of your medical bills yourself. After you’ve paid this amount, your insurance will begin to cover the remaining eligible costs according to the terms of your policy.

How can I get a cheaper visitor to Canada insurance?

Opting for plans with a higher deductible or lower coverage amount can lower premiums for a visitor in Canada policy. However, the downside is that you will have to pay the deductible amount for every emergency treatment and a lower coverage will not cover in case of a high cost medical emergency .

You can also opt for a monthly payment plan that offers more flexibility since you have to pay the premium every month instead of a lump sum amount. This can help tourists in Canada who are on a tight budget for their trip.

Which companies offer visitors to Canada insurance?

Manulife, Travelance, GMS, Destination, 21st Century and Secure Travel (RIMI) are some of the best companies that offer visitors to Canada insurance plans. Insurers such as Allianz, RIMI and Tugo also offer customized plans specifically for students in Canada.

How can I pay for Canadian visitors’ insurance?

You can pay the premium amount for visitors to Canada insurance policy in two ways: full upfront payment and monthly payment plan.

Upfront payment is straightforward, as you make a single payment at the start, which covers you for your entire trip to Canada. Many people prefer this method for its simplicity and convenience, as it eliminates the need for recurring payments and ensures uninterrupted coverage.

Monthly payment plans spread the cost of the insurance over several months. This option can be more manageable for those on a budget or with a limited cash flow, as it breaks down the total premium into smaller, more affordable installments. Insurers usually require a credit card on file for monthly payments.

Do visitors get free healthcare in Canada?

No, visitors do not get free healthcare in Canada. Although Canada has a public healthcare system, it does not extend to foreigners and non-residents visiting the country. Visitors are required to pay out-of-pocket for any medical services they may need during their stay unless they have purchased visitor medical insurance.

Without insurance, healthcare costs in Canada can be substantial — a visit to the doctor or a walk-in clinic could be anywhere from $100 to $600, while an emergency room or hospitalization could be as high as $6,000 per day!

How long do you have to live in Canada to get free healthcare?

You can receive provincial coverage after living in Canada for about three months. To qualify for free healthcare in Canada, you typically need to be a permanent resident or a citizen. After obtaining permanent residency, you can access public healthcare services as soon as you register with your provincial or territorial health insurance plan. This registration process may vary by province. During this waiting period, it is advisable to have private health insurance to cover any unexpected medical costs.

Is visitors’ insurance in Canada refundable?

Yes, in most cases, you can cancel your visitor health insurance policy and receive a refund. However, the specifics will depend on your insurance provider’s policies.

If you need to cancel your policy before coverage begins, you’re usually entitled to a full refund of the premium you paid. All policies from Canadian insurers come with a 10-day free-look period, during which you can cancel and get a full refund for any reason.

If you cancel after those 10 days, refunds are typically only given in certain cases: if your entire trip is cancelled before you arrive in Canada, if your visa is denied, if you become ineligible under the policy, or if you pass away.

Reasons you might need to cancel your visitors insurance:

Can I extend a visitor in Canada insurance plan?

Yes, you can extend a visitor in Canada insurance plan in case you are increasing your trip duration. Extending your coverage may cost extra, with premiums varying based on the extension’s duration, your age, the coverage amount, and the deductible terms.

To extend a visitors in Canada policy you must meet the following criteria:

- No claims have been submitted or intend to be submitted

- Request for extension is made before the expiration of the current policy

- Insured remains eligible for insurance, meaning they are in good health/no change in health status and are not experiencing any symptoms or planning to seek treatment during the new coverage period

- Age at the start date of extension would not make the traveller ineligible for insurance with the respective company

- Limits on the total period of coverage from the effective date of the original policy—including extensions—may also be placed by insurers, such as 1 year for GMS or 2 years for Tugo

- The required premium for the additional period of coverage is paid

Can I get insurance for visitors to Canada with a pre-existing condition?

Yes, you can get travel insurance for visitors to Canada with pre-existing health conditions. Although all insurance companies in Canada provide the pre-existing policy option, coverage may be limited.

Most companies offer two variants of policy options – one that includes pre-existing illness coverage and one that doesn’t. This ensures that young and healthy individuals can opt for visitor health insurance without pre-existing condition coverage, which has lower premiums compared to the policies covering pre-existing conditions.

However, some companies such as Allianz, GMS, Tugo, Blue Cross, and MSH International only offer visitor medical insurance with an in-built pre-existing condition coverage.

Can I pause a visitor’s insurance plan to travel back home?

Yes, you can pause a visitors to Canada insurance plan and temporarily return to your home country. This is known as a “trip break” and nearly all insurers, except GMS, allow you to pause your plan. In such cases, the policy will not terminate, but rather coverage will be suspended with no claims payable for any incidents in the insured’s home country.

It is important to note here that suspension does not mean that the clock on the policy will be paused—only coverage will be paused while the policy period will continue. In the case of a monthly payment plan, payments will continue to be made while the policy continues, even though coverage is suspended.

Can I take side trips or travel to another country on my visitors insurance?

Yes, you can take side trips and travel to another country, excluding your country of origin, while on a visitors insurance, provided your plan covers side trips. Most insurers need your side trip to originate and terminate in Canada.

Insurers such as Manulife cover side trips that do not exceed 30 days per policy or 49% of the total number of coverage days. If you take a side trip that is longer than what is permitted, your policy will be suspended while you are out of Canada. Once you return, your coverage will resume.

Do travel advisories or country restrictions affect my visitor insurance?

Yes, official travel advisories affect the side trip component of a visitors to Canada plan. Side trips are when non-residents travel outside Canada, apart from their country of origin. If you travel to a country outside Canada for which the Canadian government has issued a travel warning or advisory, you will not be covered for any illness or injury that may have occurred in that region. In some cases, your policy might be terminated if you travel to a country for which the government has issued an advisory.

Looking for the best visitor insurance plan? Speak to our expert advisors!

If you’re looking for visitors insurance to Canada and not sure where to start, contact us now! Our team of expert insurance advisors would be happy to go over the unique needs of your trip and give you personalized advice for the kind of policy that would be best for you. Schedule a call or start comparing customized quotes right away by clicking the button below.

Frequently Asked Questions

Do visitors’ insurance plans require a medical examination?

No, visitors’ insurance plans typically do not require a medical examination. Insurers may require a health questionnaire or declaration about pre-existing conditions, which helps them assess risk and determine coverage options.

Can I visit Canada without health insurance?

Yes, you can visit Canada without health insurance for visitors. But it is highly recommended that you get a visitors insurance plan to avoid paying exorbitant amounts for emergency medical treatment while you are in Canada.

Can non-Canadian residents get free healthcare?

No. Non-residents in Canada do not have access to provincial healthcare. Only citizens and permanent residents are covered under Canada’s provincial healthcare.

Which is the best visitor insurance company in Canada?

Manulife, Tugo, GMS, Destination, Allianz, 21st Century, Secure Travel and Travelance are some of the top insurance companies in Canada that offer visitors to Canada insurance plans.

Visitor insurance is designed to offer emergency medical coverage for individuals visiting Canada, including tourists, international students, and temporary workers. Plans typically cover a range of medical expenses, including hospital stays, emergency medical transportation, and outpatient care. Some policies may also include additional benefits like trip cancellation, lost baggage, and personal liability coverage.